Peer effects on ESG performance of resource-based enterprises: based on vertical and horizontal networks

0

0 Abstract

This paper empirically examines the existence and influence mechanisms of peer effects on ESG (Environmental, Social, and Governance) performance under vertical and horizontal networks, using a sample of Chinese A-share listed resource-based enterprises from 2012 to 2023. The study finds that under the interactive effects of both vertical and horizontal networks, there is a significant peer effect in enterprises’ ESG outcomes. Moreover, this effect primarily influences a focal enterprise through “end-treatment” and “front-prevention”. Further research reveals that due to differences in improvement motivations, supply chain discourse power, and driving networks, the peer effect in ESG performance exhibits heterogeneity. This paper provides theoretical and empirical support for enterprises to enhance their ESG performance within complex supply chain networks, which is of great significance for promoting sustainable development of firms.

Keywords

INTRODUCTION

With the popularization of ESG (Environmental, Social, and Governance) evaluation standards, integrating them into supply chain management has become an essential strategy for enterprises to enhance their competitiveness and strengthen supply chain stability. The comprehensive performance of enterprises in the ESG domain not only reflects their sense of social responsibility but also serves as the cornerstone for achieving long-term sustainable development[1]. Excellent ESG performance helps enterprises better cope with risks in a complex and ever-changing environment, thereby achieving steady development. In the context of green development, the decisions of enterprises are not only driven by internal factors but also influenced by the behaviors of external enterprises, a phenomenon known as “peer effects”. Positive peer effects imply positive interactions and collaborative improvements among enterprises. This effect may drive the collective progress of the entire industry in ESG performance through mechanisms such as information sharing, resource complementarity, and competitive cooperation. To fully comprehend this dynamic relationship, it is necessary to delve into how the ESG performance of peer enterprises influences that of focal enterprises through supply chain transmission, both theoretically and practically.

Enterprises do not operate in isolation when making decisions; rather, they frequently draw upon and reference the decisions of their peers[2]. Ali-Rind et al. (2023)[3] underscore the pivotal significance of peer effects in sculpting corporate behavior across a diverse array of domains. Globalization’s progress has refined the industrial division of labor, fostering closer ties among supply chain’s upstream and downstream enterprises and giving rise to a complex supply chain network[4]. This network includes both “vertical peer groups” (upstream and downstream enterprises) and “horizontal peer groups” (enterprises sharing customers or suppliers with the focal enterprise).

Within vertical supply chain networks, enterprises forge strong connections with both upstream suppliers and downstream customers[5]. This is evident not only in the movement of materials and information but also in the spillover of ESG performance[6]. Specifically, when an enterprise excels in ESG, this positive impact can ripple through the supply chain and subsequently enhance sustainability across the entire network[7,8]. Meanwhile, dominant enterprises, which possess greater influence within the supply chain, are more apt to leverage their position so as to drive up ESG performance throughout the supply chain[9]. Thus, this vertical peer effect fully highlights the deep interdependence and close connectivity among enterprises within the supply chain network.

In horizontal supply chain networks, enterprises operating in the same industry demonstrate significant industry peer effects concerning corporate social responsibility performance, ESG disclosure, and overall ESG performance. This is because they operate in similar market environments, face comparable industry prospects, and share analogous customer bases[10-14]. Moreover, the interplay of specific cultural, policy, and economic factors leads to a noticeable convergence in ESG performance among enterprises within the same geographical region[15]. This horizontal peer effect highlights the impact of industry and regional dynamics on enterprise ESG performance.

However, the existing literature on the peer effects of ESG performance mainly adopts a unilateral analytical approach, focusing either on vertical or horizontal networks in isolation. Such an approach tends to neglect the complexity and integrated nature of supply chain networks, potentially yielding conclusions that lack systematic and all-encompassing insights. Therefore, this paper constructs a framework that combines the analysis of both vertical and horizontal networks, with the aim of comprehensively explaining the propagation mechanisms of ESG performance within supply chain networks. Furthermore, resource-based enterprises, which heavily depend on natural resources for their production and operations, are confronted with a host of formidable challenges. These encompass stricter environmental regulatory pressures, elevated social responsibility expectations, and the perils of resource depletion and escalating market competition. In such a context, the peer effects associated with ESG performance are likely to assume a more prominent role, providing vital support for these enterprises to bolster their resilience within a complex operational landscape.

Consequently, this study chooses Chinese A-share listed resource-based enterprises as the research sample, with the objective of conducting an in-depth exploration of the channels via which the ESG performance of peer enterprises impacts that of focal enterprises. Through empirical analysis, this paper uncovers the existence and intrinsic mechanisms of peer effects on ESG performance among resource-based enterprises within both vertical and horizontal networks. In comparison with existing literature, the marginal contributions of this study are evident in the following respects:

Firstly, previous research has mainly restricted its focus to single-tier networks, neglecting the intricate reality that enterprises function within a web of interconnected vertical and horizontal networks. In contrast, this study takes a dual-network approach, surpassing the constraints of existing single-tier analyses and broadening the investigation into the factors influencing enterprise ESG practices.

Secondly, this paper makes an in-depth exploration of the operational mechanisms of peer effects, pinpointing two main pathways - “end-treatment” and “front-prevention” - through which these effects materialize. This discovery not only furnishes new theoretical foundations for comprehending the transmission mechanisms of peer effects but also provides fresh analytical viewpoints for enterprises aiming to improve their ESG performance.

The structure of this study unfolds as follows. Section 2 engages in theoretical analysis and puts forward research hypotheses. Section 3 describes the research design. Section 4 displays the results. Finally, section 5 concludes the paper.

THEORETICAL ANALYSIS AND RESEARCH HYPOTHESIS

The existence of peer effects on ESG performance within vertical and horizontal networks

Social network theory sheds light on how information, resources, and behavioral patterns spread among members within a network, leading to the emergence of peer effects. These effects are equally discernible in the context of enterprise ESG performance. When some enterprises in a network exhibit outstanding ESG performance, their actions and accomplishments frequently act as reference points for other enterprises to learn from and follow. Within the complex tapestry of supply chain networks, marked by both vertical and horizontal connections, no enterprise operates in a vacuum. Rather, each enterprise is intricately linked to others through diverse channels, such as supply chain relationships, inter-industry competition, and cooperation.

Within vertical networks, the exchange of resources, technologies, and knowledge among enterprises cultivates mutual interactions. Alterations in one supply chain entity frequently prompt corresponding adaptations from other entities within the network[16]. Notably, stakeholders are instrumental in motivating enterprises to embrace higher standards of corporate social responsibility[17]. The commendable ESG performance of upstream and downstream enterprises conveys expectations for elevated ESG standards to focal enterprises via supply chain relationships[18,19]. To fulfill these expectations, sustain business ties, and preserve market competitiveness, focal enterprises generally respond proactively by endeavoring to elevate their own ESG performance[20-22]. Simultaneously, the supply chain network furnishes a social capital foundation for enterprises to generate sustainable value. Enterprises with outstanding ESG performance propagate green practices throughout the supply chain, thereby fostering comprehensive green development across the entire network[21]. Moreover, in accordance with signaling theory, superior ESG performance enhances an enterprise’s reputation and image, drawing in higher-caliber resources. This information disseminates swiftly through the supply chain, spurring imitation and learning behaviors among other enterprises. As a result, the ESG performance of focal enterprises is substantially influenced by the ESG performance of other enterprises within the supply chain network, engendering peer effects.

In horizontal networks, enterprises’ ESG performance is profoundly shaped by dynamic competition theory. When devising strategies, enterprises keenly observe and react to the moves of their rivals[22,23]. Especially in the current developmental phase, with inter-enterprise interactions becoming ever more intricately linked, enterprises display heightened awareness of their competitors’ green endeavors[24,25]. When competitors showcase exemplary ESG performance, other enterprises frequently sense pressure from the market and investors, compelling them to revise their strategies to meet market expectations, ultimately resulting in a convergence of ESG performance[26]. From the vantage point of social comparison theory, enterprises typically gauge their market standing and performance by benchmarking themselves against peers within the same industry. To maintain their viability amidst intense competition, managers dynamically adapt their decisions in response to the actions of peer enterprises[27]. Upon witnessing remarkable ESG accomplishments by other industry participants, enterprises may feel inspired to follow suit and learn from them, with the aim of enhancing their own image and market competitiveness. Moreover, empirical research indicates that superior ESG performance substantially elevates a firm’s overall value[28] and stock returns[29]. Consequently, propelled by profit motives, enterprises are more inclined to enhance their ESG performance, as this not only fortifies their market competitiveness but also aids in attracting investor preference. Collectively, these factors contribute to the phenomenon of ESG performance convergence among enterprises within horizontal networks.

The preceding analysis centered on single-layer networks, either vertical or horizontal, to clarify the peer effects on ESG performance. In actuality, enterprises are influenced by peer effects resulting from the synergistic combination of vertical and horizontal networks, with coupled dynamics between the two types of peer effects.

On the one hand, the intensification of horizontal peer effects indicates increased industry competition[30]. In a more competitive setting, firms’ imitative behaviors become more evident[31]. This competitive strain not only compels enterprises to improve their own ESG performance but also encourages them to prioritize stable relationships with vertical supply-chain partners[32], leading to the formation of tighter collaborative networks[33]. It is worth noting that superior ESG performance not only enables enterprises to build a more favorable social image but also strengthens relational trust with upstream and downstream partners[34]. To satisfy the expectations of supply-chain partners for high ESG standards, enterprises need to align their ESG performance with that of their vertical peers[35]. Besides, information-sharing mechanisms among horizontal peers can enhance the understanding of ESG principles and practices among enterprises along the vertical chain, thus boosting their enthusiasm for adopting and implementing ESG strategies. Furthermore, since horizontal peers often share customers and suppliers, the improvement of industry-wide ESG performance generates a normative force that raises ESG performance expectations in upstream and downstream sectors, urging vertical enterprises to speed up their ESG enhancements. On the other hand, when enterprises across the vertical supply chain uniformly adopt and raise ESG standards, this sets industry-level norms that influence horizontal peers sharing customers or suppliers with focal enterprises. Moreover, when upstream and downstream enterprises impose ESG requirements, those with superior ESG performance are more likely to secure stable supply-chain partnerships. This advantageous position transfers competitive pressures from vertical peer effects to other enterprises within the same industry, forcing horizontal peers to further upgrade their ESG performance to maintain market competitiveness and supply chain stability.

Based on the analysis, this paper proposes the first research hypothesis:

H1: Under the synergistic influence of vertical and horizontal networks, there exists a peer effect on enterprises’ ESG performance.

Influence mechanisms of peer effects on ESG performance

To tackle the peer effects on ESG performance, focal enterprises can improve their ESG performance via two main strategies: “end-treatment” and “front-prevention”. Compared with front-prevention, end-treatment and practices akin to “greenwashing” generally involve lower costs[36]. Focal enterprises can swiftly enhance their ESG performance in the short run by ramping up environmental protection investments, procuring advanced pollution control equipment, or setting up resource recycling and utilization facilities. These initiatives augment pollutant treatment capabilities and lower carbon emission intensity, allowing enterprises to promptly meet the high ESG standards set by horizontal peers and swiftly respond to ESG requirements from suppliers or clients, thereby safeguarding collaborative ties. Nevertheless, after attaining short-term ESG enhancements through end-treatment, enterprises need to place greater emphasis on long-term development. They should innovate production processes, develop environmentally friendly technologies, enhance green innovation capabilities, and reinforce front-prevention measures. This enables them to continuously optimize resource utilization efficiency and pollution control, ensuring sustained and robust ESG performance over the long haul.

Environmental investments and green innovation exert a positive impact on the ESG performance of focal enterprises[37]. Firstly, they substantially elevate environmental performance. Through the adoption of cutting-edge technologies and equipment, enterprises can curtail carbon emissions, optimize resource utilization, and reduce pollution levels[38]. Secondly, they enhance the enterprise’s social image. Incorporating environmental principles into governance frameworks not only bolsters social performance[13] but also deepens public acknowledgment of the enterprise’s social responsibility. Finally, environmental investments and green innovation necessitate robust governance systems to guarantee rational resource allocation and efficient project implementation. This fosters scientific decision-making and refines governance mechanisms[39].

Thus, as vital instruments for sustainable development, both end-treatment and front-prevention, when combined with increased environmental investments and green innovation, propel comprehensive improvements in ESG performance.

Based on the analysis, this paper proposes the second research hypothesis:

H2: Under the synergistic influence of vertical and horizontal networks, peer effects on ESG performance can enhance focal enterprises’ ESG performance by elevating their “end-treatment” and “front-prevention” capabilities.

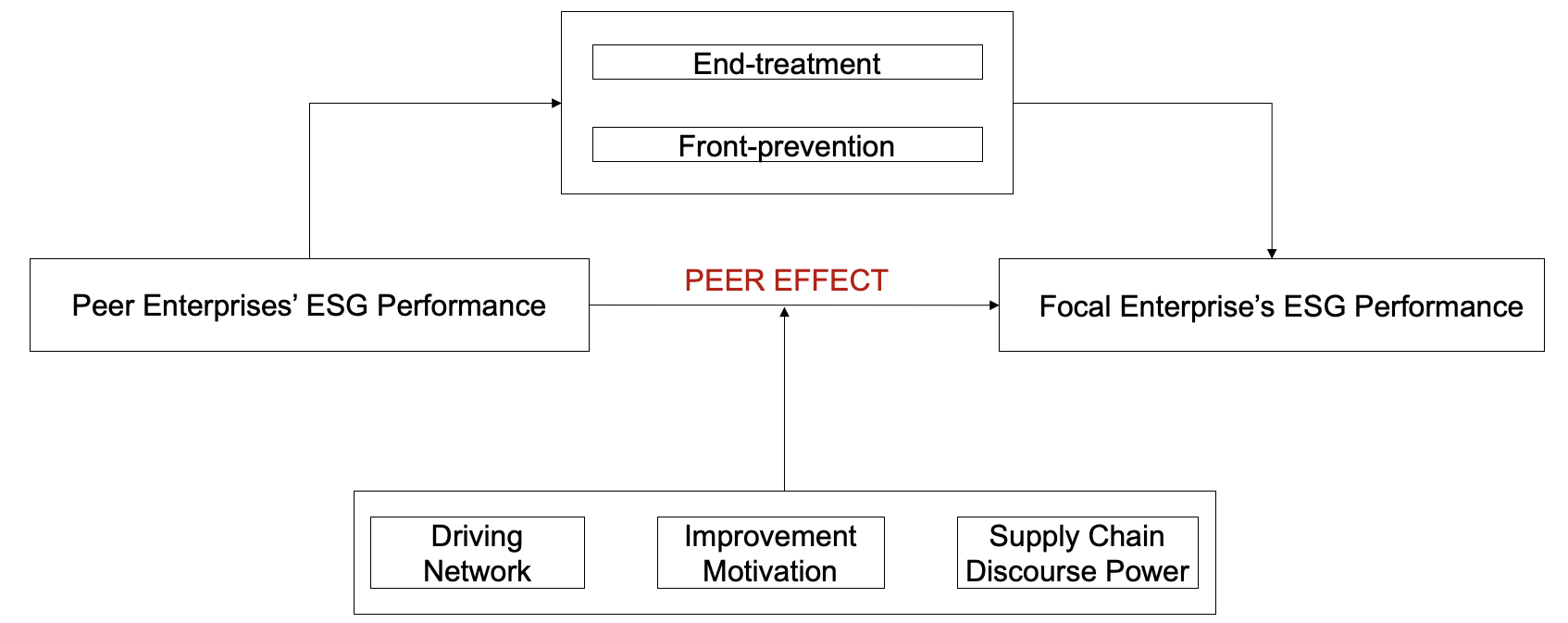

Figure 1 constructs a theoretical framework for the peer effect on ESG performance.

Figure 1. Theoretical framework for the peer effect on ESG performance. ESG: Environmental, social, and governance.

RESEARCH DESIGN

Sample selection and data source

This research takes Chinese A-share listed resource-based enterprises spanning from 2012 to 2023 as its research sample. The original data is obtained from the WIND Database (https://www.wind.com.cn/) and the China Stock Market & Accounting Research (CSMAR) Database (https://data.csmar.com/). To bolster the validity of parameter estimation, the original data is processed through the following steps: First, firms classified as financial institutions and those with incomplete data records are eliminated from the sample. Second, companies marked as ST or *ST are excluded on account of their financial instability or irregularities. Third, companies with missing or negative values for crucial financial indicators are removed to uphold data integrity. Finally, to reduce the influence of extreme or outlier values on the estimation results, all continuous variables are winsorized at the 1% and 99% levels.

Variable declaration

Dependent variable: ESG performance (ESG)

This study adopts the Huazheng ESG Rating to measure the ESG performance of focal enterprises. The ESG ratings, ranging from AAA to C, are numerically assigned values from 9 to 1, with higher scores indicating superior ESG performance.

Independent variable: peer enterprises’ ESG performance (Peer_ESG)

First, the mean ESG performance of all enterprises in the same industry, excluding the focal enterprise, is employed as a proxy for the horizontal peer ESG influence (Horizontal_ESG). Second, with regard to vertical peer influence, this study pinpoints the top five publicly listed suppliers and customers of the focal enterprise that have no affiliation with it. The ESG performance of these vertical peers is then weighted according to the total transaction volume with the focal enterprise to calculate Vertical_ESG. Finally, to grasp the synergistic impact of both horizontal and vertical peer ESG effects, the product of Horizontal_ESG and Vertical_ESG is computed. This multiplicative indicator mirrors the combined influence of industry peers and supply chain partners on the focal enterprise’s ESG performance.

Mechanism variables: end-treatment (Invest) and front-prevention (Innovation)

Drawing on the methodological approaches adopted by Xiao et al. (2023)[39], this study employs the magnitude of environmental protection investment (Invest) as a metric for “end-treatment” and the extent of green innovation (Innovation) as an indicator for “front-prevention”. Specifically, the amount of investment related to environmental protection disclosed by enterprises in the current fiscal year is used to assess their environmental protection investment. Considering the inherent time lag associated with patent grant data, the count of green patent applications offers a more timely and intuitive representation of an enterprise’s level of green technological innovation. As a result, the natural logarithm of the number of green patent applications is taken as the measure for quantifying an enterprise’s green technological innovation.

Control variables

This paper uses firm size (Asset), financial leverage (Lev), cash flow (Cash), return on assets (ROA), growth (Grow), Tobin’s Q (TQ), dual role of the chairman and CEO (Duty), and board size (Board) as control variables at the firm level. Additionally, the analysis controls for year- and industry-fixed effects.

Model construction

To examine the existence and underlying mechanisms of peer effects on enterprises’ ESG performance, this study employs a panel data regression model with year- and industry-fixed effects to control for unobserved time-varying and industry-specific heterogeneities. The model is specified as follows:

where ESG represents the ESG performance of the focal enterprise; Peer_ESG indicates the ESG performance of peer enterprises within the horizontal and vertical networks; Invest denotes the level of environmental protection investment of the focal enterprise; Innovation stands for the level of green innovation of the focal enterprise; Controls signify a series of control variables; Year and Ind correspond to year- and industry-fixed effects, respectively; and ε represents the stochastic error term.

RESULTS

The existence of peer effects on ESG performance

Table 1 reports the test results on the impact of peer enterprises’ ESG performance on that of focal enterprises. In column (1), which controls only for year and industry fixed effects, the coefficient of Peer_ESG is 0.535 and is significant at the 1% level. After incorporating a series of firm-level control variables, the regression results are shown in column (2), where the coefficient of Peer_ESG is 0.456 and remains positive and significant at the 1% level. The empirical results indicate a significant positive correlation between Peer_ESG and ESG, further confirming the existence of peer effects on ESG performance. This finding suggests that enterprises are influenced by their peers in terms of ESG performance and tend to imitate and adopt similar strategies and behaviors[40]. Hypothesis H1 is thus verified.

Baseline regression results

| (1) | (2) | (3) | (4) | (5) | |

| ESG | ESG | E | S | G | |

| Peer_ESG | 0.535*** | 0.456*** | |||

| (0.065) | (0.062) | ||||

| Peer_E | 0.179** | ||||

| (0.075) | |||||

| Peer_S | 0.420*** | ||||

| (0.091) | |||||

| Peer_G | 0.228*** | ||||

| (0.068) | |||||

| Asset | 0.307*** | 0.245*** | 0.318*** | 0.300*** | |

| (0.036) | (0.035) | (0.058) | (0.044) | ||

| Lev | -1.770*** | -0.529** | -2.148*** | -1.904*** | |

| (0.249) | (0.239) | (0.401) | (0.303) | ||

| Cash | 0.045 | -0.041 | -0.019 | 0.165*** | |

| (0.044) | (0.043) | (0.072) | (0.054) | ||

| ROA | -0.240 | -0.881 | -0.186 | 0.071 | |

| (0.675) | (0.648) | (1.086) | (0.822) | ||

| Grow | 0.265 | -0.039 | 0.374 | 0.111 | |

| (0.168) | (0.162) | (0.270) | (0.204) | ||

| TQ | 0.016 | -0.030 | -0.026 | 0.041 | |

| (0.040) | (0.038) | (0.064) | (0.049) | ||

| Duty | -0.002 | -0.002 | -0.005 | 0.000 | |

| (0.004) | (0.004) | (0.007) | (0.005) | ||

| Board | -0.098 | 0.135 | 0.253 | -0.355 | |

| (0.181) | (0.175) | (0.292) | (0.221) | ||

| Constant | 1.680*** | -3.933*** | -4.127*** | -4.382*** | -1.168 |

| (0.265) | (0.831) | (0.801) | (1.330) | (1.018) | |

| Year FE | No | Yes | Yes | Yes | Yes |

| Industry FE | No | Yes | Yes | Yes | Yes |

| N | 878 | 878 | 878 | 878 | 878 |

| R2 | 0.171 | 0.279 | 0.173 | 0.182 | 0.311 |

Furthermore, this paper delves into the disaggregated analysis of each dimension of ESG. The results, as illustrated in columns (3) to (6), reveal that the impact coefficients of peer enterprises’ performance in the environmental (E), social (S), and governance (G) dimensions on the focal enterprises are 0.179, 0.420, and 0.228, respectively, with all coefficients being statistically significant at the 5% level. These findings indicate that peer enterprises’ performance in each subdivided dimension of ESG exerts a significant influence on the focal enterprise.

The empirical results shed light on the specific mechanisms through which peer effects operate across different ESG dimensions. In the environmental dimension, peer enterprises’ proactive environmental strategies can inspire the focal enterprise to increase its investment in environmental protection and enhance its environmental performance. On the social dimension, peer enterprises’ exemplary practices in fulfilling social responsibilities serve as a model for the focal enterprise, prompting it to place greater emphasis on social responsibility. In the governance dimension, peer enterprises’ efficient enterprise governance structures and mechanisms offer valuable references for the focal enterprise, helping it to improve its own governance standards.

In summary, the disaggregated analysis of ESG dimensions demonstrates that peer enterprises’ performance in each dimension has a discernible impact on the focal enterprise. This insight not only enriches our understanding of the multifaceted nature of ESG peer effects but also provides practical guidance for firms seeking to leverage peer effects to enhance their ESG performance across different dimensions.

Robustness tests

Change in sample period

To exclude the impact of the coronavirus (COVID-19) pandemic, this paper opts to exclude data from after 2020 and conducts the regression analysis again. The regression results, as shown in column (1) of Table 2, further validate the robustness of our conclusions.

Robustness tests

| (1) | (2) | (3) | (4) | (5) | (6) | |

| ESG | ESG | ESG | E | S | G | |

| Peer_ESG | 0.482*** | 0.619*** | 0.467*** | |||

| (0.074) | (0.061) | (0.068) | ||||

| Peer_E | 0.324*** | |||||

| (0.084) | ||||||

| Peer_S | 0.362*** | |||||

| (0.120) | ||||||

| Peer_G | 0.252*** | |||||

| (0.079) | ||||||

| Constant | -4.207*** | -4.553*** | 8.537 | 9.556 | 11.750 | 29.977*** |

| (1.026) | (0.814) | (6.203) | (7.141) | (11.725) | (7.602) | |

| Controls | Yes | Yes | Yes | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes | Yes | Yes | Yes |

| N | 665 | 878 | 878 | 878 | 878 | 878 |

| R2 | 0.270 | 0.314 | 0.287 | 0.249 | 0.139 | 0.321 |

Modifying the measurement of peer effect

Common types of horizontal peer effects primarily include industry peers and regional peers[41]. Specifically, enterprises within the same industry face similar market environments, industry prospects, and customer bases, while enterprises in the same region operate within identical political, economic, and cultural contexts, leading to convergence in their business decisions. In the baseline regression analysis, this paper employs the average ESG performance of other enterprises in the same industry (excluding the focal enterprise) in the same year as a metric for the horizontal peer enterprises’ ESG performance. In the robustness test section, we instead use the average ESG performance of other enterprises in the same province and year to measure the ESG performance of horizontal peer enterprises. The results, as shown in column (2) of Table 2, indicate that the findings from the robustness test are consistent with those from the baseline regression, further supporting hypothesis H1.

Modifying the measurement of ESG

Huazheng provides core ESG scores and ratings, offering an important basis for evaluating enterprises’ ESG performance. In the baseline regression analysis, this paper uses ESG ratings to assess firms’ ESG outcomes. In the robustness test, we instead use the annual ESG scores from Huazheng’s rating system to measure firms’ ESG performance. The empirical results, as illustrated in columns (3) to (6) of Table 2, verify the robustness of the previous conclusions.

Propensity score matching method

To mitigate the impact of differences in characteristics among listed companies, this paper employs the propensity score matching method for regression analysis. Based on the average ESG performance of peer enterprises, we divide the sample enterprises into a “high peer effect group” and a “low peer effect group”, using the control variables mentioned earlier as matching variables. Logit regression is utilized to calculate the propensity matching scores, and samples are matched using a 1-to-1 nearest neighbor matching method with replacement. The matched samples pass the balance test and the common support assumption test, ensuring the reliability and validity of the matching. The matched samples are then substituted back into model (1) for regression, and the results are shown in Table 3. Specifically, column (1) presents the regression results before matching, while column (2) displays the results after matching. The empirical results indicate that after matching, the regression coefficient of peer enterprises’ ESG performance on that of the focal enterprise remains significantly positive at the 1% level. The empirical findings suggest that after accounting for sample selection bias, the research conclusions presented earlier remain unchanged, further validating the robustness of the baseline regression results.

Propensity score matching method

| (1) | (2) | |

| ESG | ESG | |

| Peer_ESG | 0.456*** | 0.446*** |

| (0.062) | (0.062) | |

| Constant | -3.933*** | -3.971*** |

| (0.831) | (0.842) | |

| Controls | Yes | Yes |

| Year FE | Yes | Yes |

| Industry FE | Yes | Yes |

| N | 878 | 871 |

| R2 | 0.279 | 0.286 |

Endogeneity discussion

To address potential issues of bidirectional causality and endogeneity, this paper further constructs instrumental variables and employs a two-stage least squares (2SLS) method for testing. Drawing on the research of Adhikari and Agrawal (2018)[41], this paper selects the average idiosyncratic stock return (IV1) of peer enterprises as the first instrumental variable. Firstly, enterprises with excellent ESG performance are generally perceived to possess higher ethical standards and more sustainable business models, making them more attractive to investors and thus exhibiting higher idiosyncratic stock returns. This satisfies the relevance requirement for instrumental variables. Secondly, for the focal enterprise, the average idiosyncratic stock return and volatility of its peer enterprises are only correlated with its own ESG performance and do not directly influence the ESG performance of the focal enterprise, meeting the exogeneity condition for instrumental variables. Additionally, this paper selects the lagged ESG performance of peer enterprises (IV2) as the second instrumental variable.

Based on this, this paper applies the 2SLS method for testing, and the regression results are presented in Table 4. Columns (1) and (2) in Table 4 display the first-stage regression results of the instrumental variable method. It can be observed that both instrumental variables are significant at the 1% significance level, indicating a significant correlation between the instrumental variables and the endogenous variable. Column (3) presents the second-stage regression results of the instrumental variable method. The results show that after accounting for potential endogeneity issues, the ESG performance of the focal enterprise remains significantly positive at the 1% significance level, implying that the ESG performance of peer enterprises still significantly promotes that of the focal enterprise. Furthermore, this paper conducts tests on the validity of the instrumental variables. The F-value of the weak instrumental variable test exceeds all critical values, suggesting the absence of a weak instrumental variable problem. The P-value of the Kleibergen-Paap rk LM statistic is 0.000, indicating a strong correlation between the instrumental variables and the endogenous variable. Meanwhile, the P-value of the Hansen test is significantly greater than 10%, suggesting that the selected instrumental variables pass the over-identification test and possess high reliability. Overall, by controlling for potential endogeneity issues, the empirical results indicate that the ESG performance of peer enterprises has a significant promoting effect on that of the focal enterprise. This conclusion once again validates the robustness of the research findings in this paper.

Instrumental variables

| (1) | (2) | (3) | |

| ESG | ESG | ESG | |

| IV1 | 0.717*** | ||

| (0.271) | |||

| IV2 | 0.399*** | ||

| (0.047) | |||

| Peer_ESG | 0.808*** | ||

| (0.215) | |||

| Constant | 3.352*** | 2.046*** | -5.357*** |

| (0.418) | (0.598) | (1.244) | |

| Controls | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes |

| N | 878 | 467 | 467 |

| R2 | 0.104 | 0.254 | 0.218 |

Mechanism tests

This paper references the mediation effect testing method proposed by Jiang et al. (2022)[42]. Based on the regression results of model (1), we further examined the mediating effects of “end-treatment” and “front-prevention” through model (2). Column (1) of Table 5 presents the impact of peer enterprises’ ESG performance on the focal enterprise’s ESG performance. Columns (2) and (3) respectively display the empirical results of peer enterprises’ ESG performance on “end-treatment” and “front-prevention”. The study reveals that the coefficients of Peer_ESG are significantly positive at the 5% level, indicating that peer enterprises’ ESG performance has a significant promoting effect on both “end-treatment” and “front-prevention”. According to the principles of mediation effect testing, it can be inferred that peer enterprises’ ESG performance effectively enhances that of the focal enterprise by promoting its “end-treatment” and “front-prevention”. Consequently, Hypothesis H2 is validated.

Mechanism tests

| (1) | (2) | (3) | |

| ESG | Invest | Innovation | |

| Peer_ESG | 0.456*** | 0.767*** | 0.066** |

| (0.062) | (0.258) | (0.028) | |

| Constant | -3.933*** | -13.529*** | -0.082 |

| (0.831) | (3.791) | (0.114) | |

| Controls | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes |

| N | 878 | 878 | 878 |

| R2 | 0.279 | 0.315 | 0.135 |

Heterogeneity tests

Different improvement motivations

This paper argues that there are differences in the motivations of focal enterprises to improve their ESG performance influenced by peer effects, which can be categorized into proactive improvement motivations and passive response motivations. Focal enterprises with proactive improvement motivations possess strong endogenous driving forces, and their actions to enhance ESG performance are aimed at achieving their own sustainable development goals and maintaining long-term competitive advantages. In contrast, focal enterprises with passive response motivations are more inclined to signal their alignment with ESG development trends to the outside world, thereby maintaining relative competitive advantages with lateral peer enterprises and fostering cooperative relationships with vertical peer enterprises. This paper draws on the research by Lu and Hu (2024)[43], stating that if the focal enterprise’s ESG performance in the previous period was superior to that of its peer enterprises, it is classified into the proactive group; conversely, it is classified into the reactive group. Secondly, the absolute value of the difference between the focal enterprise’s ESG performance and the average ESG performance of its peer enterprises (|ESG - Peer_ESG|) is calculated and substituted into model (1) for regression analysis.

Columns (1) and (2) of Table 6 present the regression results for the proactive and reactive groups, respectively, addressing whether there are differences in the motivations for the focal enterprise’s improvement in ESG performance. The research findings indicate that the motivations for the focal enterprise’s improvement in ESG performance include both proactive and reactive types. Further, columns (3) and (4) present the regression results for the proactive and reactive groups based on model (1), respectively. The study finds that enterprises in the proactive group do not show significant reactions to the ESG performance of their peer enterprises, whereas enterprises in the reactive group are significantly driven by the ESG performance of their peer enterprises. This difference may stem from the distinct intrinsic driving forces and behavioral patterns of the two types of enterprises. Specifically, enterprises in the proactive group are typically capable of proactively planning and advancing ESG improvement strategies without waiting for the manifestation of peer effects. The relative gap with their peer enterprises itself becomes a driving force for them to accelerate the improvement of their ESG performance. In contrast, enterprises in the reactive group adopt a wait-and-see attitude towards improving their ESG performance and often rely on the practical experiences of their peer enterprises as reference points before taking actual actions to promote improvements in their ESG performance.

Heterogeneity tests

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | |

| ESG | ESG | ESG | ESG | ESG | ESG | ESG | |

| Peer_ESG | 0.653*** | 0.347*** | 0.358*** | ||||

| (0.099) | (0.104) | (0.069) | |||||

| |ESG - Peer_ESG| | 0.297 | 0.447*** | |||||

| (0.069) | (0.041) | ||||||

| Vertical_ESG | 0.325*** | ||||||

| (0.033) | |||||||

| Horizontal_ESG | 0.289* | ||||||

| (0.162) | |||||||

| DP × Peer_ESG | 0.426*** | ||||||

| (0.138) | |||||||

| DP | -1.725*** | ||||||

| (0.578) | |||||||

| Constant | -2.630* | -2.180 | -0.308 | -0.091 | -3.729*** | -3.315*** | -3.341*** |

| (1.428) | (1.604) | (1.499) | (1.316) | (1.053) | (0.796) | (0.850) | |

| Controls | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| N | 200 | 267 | 200 | 267 | 878 | 878 | 878 |

| R2 | 0.450 | 0.355 | 0.378 | 0.549 | 0.235 | 0.310 | 0.287 |

Different driving networks

In the baseline regression section of this paper, we discussed the existence of peer effects on ESG performance within both vertical and horizontal networks. Here, we will further explore whether the driving source of the peer effects on ESG performance originates from vertical networks or horizontal networks. We substitute Peer_ESG with the ESG performance of peer enterprises in the vertical network (Vertical_ESG) and in the horizontal network (Horizontal_ESG), respectively, and substitute them into model (1) for regression analysis. Columns (5) and (6) of Table 6 present the regression results for the vertical and horizontal networks, respectively. The coefficient of Vertical_ESG is positive and significant at the 1% level, while the coefficient of Horizontal_ESG is positive and significant at the 10% level. The empirical results indicate that, compared with the horizontal network, peer effects within the vertical network have a more pronounced impact on improving enterprises’ ESG performance. The possible reason is that, under the vertical network, the mutual influence and learning among enterprises are closer, information sharing and resource collaboration are more frequent, and cooperation mechanisms based on interest-driven incentives are more likely to form peer effects. In contrast, due to market competition and information barriers among enterprises in the horizontal network, their peer effects are relatively weaker. Therefore, greater emphasis should be placed on fostering cooperative relationships with upstream and downstream enterprises in the supply chain to maximize the peer effects brought about by the vertical network, thereby promoting the continuous improvement of enterprises’ ESG performance.

Supply chain discourse power

Supply chain discourse power reflects an enterprise’s core competitiveness. When an enterprise holds significant discourse power within the supply chain, it can better understand and control risk factors within the supply chain, enabling the enterprise to anticipate and respond to potential disruptions and delays in delivery. Additionally, higher discourse power allows enterprises to establish closer cooperative relationships with suppliers. This collaboration not only helps mitigate supply chain risks but also enhances the overall efficiency and responsiveness of the entire supply chain. Overall, supply chain discourse power plays a crucial role in strengthening an enterprise’s risk management capabilities. It not only assists enterprises in more comprehensively assessing risks and establishing effective early warning systems but also enables them to formulate more effective risk response measures and strengthen cooperation with suppliers.

Therefore, this paper, referencing the work by Li et al. (2024)[9], measures an enterprise’s supply chain discourse power (DP) by taking the average of the sum of the procurement and sales ratios of the top five suppliers and top five customers of the focal enterprise. When a firm’s bargaining power in the supply chain exceeds the median, DP is assigned a value of 1; otherwise, it is assigned a value of 0. In Column (7) of Table 6, the estimated coefficient of the interaction term DP × Peer_ESG is significantly positive. The results indicate that the impact of peer effects on ESG performance is more pronounced in the sample group with relatively high supply chain discourse power.

RESEARCH CONCLUSIONS AND IMPLICATIONS

Based on sample data of Chinese A-share listed resource-based enterprises from 2012 to 2023, this paper systematically examines the existence and influence mechanism of peer effects in enterprise ESG performance under the interplay of vertical and horizontal networks. The study finds that under the interaction of vertical and horizontal networks, there is a significant peer effect in enterprise ESG performance. Specifically, the peer effect exhibits significant characteristics across the three dimensions of environment, society, and governance, indicating that the outstanding performance of peer enterprises in various ESG dimensions has a significant demonstration effect on focal enterprises, thereby promoting continuous improvements in environmental management, social responsibility fulfillment, and enterprise governance structures of focal enterprises.

Further research reveals that the peer effect in ESG performance under vertical and horizontal networks mainly influences focal enterprises’ ESG performance through two pathways: “end-treatment” and “front-prevention”. The synergistic effects of these dual pathways of governance and prevention not only provide effective avenues for focal enterprises to achieve ESG improvements but also offer theoretical support for the transmission mechanism of peer effects.

Additionally, the study finds that the peer effect in ESG performance exhibits significant heterogeneity. Specifically, due to the differences in improvement motivations, supply chain discourse power, and driving networks, the intensity and mode of action of peer effects vary. This research provides a new theoretical perspective for understanding the dynamic evolution of enterprise ESG performance under vertical and horizontal networks, while also offering empirical support for enterprises to enhance their risk resistance capabilities through ESG collaboration in complex environments. The research conclusions hold significant practical implications for promoting enterprise sustainable development.

Based on the above findings, this paper proposes the following implications:

First, leverage the peer effects of ESG performance. The government should improve the supervisory mechanism for ESG information disclosure, promoting enterprises to enhance the transparency and quality of ESG information disclosure, thereby laying the foundation for inter-enterprise learning and benchmarking. It should also actively guide and support organizations such as industry associations to play a bridging role, establishing communication platforms among enterprises to facilitate the exchange and cooperation of ESG experiences, and fostering a favorable atmosphere for ESG peer effects. Additionally, the government needs to formulate and complete ESG-related policies and standards, clarifying enterprises’ responsibilities and obligations in environmental, social, and governance aspects, providing enterprises with clear action guidelines. Meanwhile, it should conduct regular assessments and supervision of enterprises’ ESG performance to ensure that their performance in various dimensions meets industry standards and encourage enterprises to learn from outstanding benchmarks within their peer group, continuously improving their ESG management capabilities. Through multi-party collaboration, the peer effects of ESG can be effectively stimulated, driving an overall improvement in enterprises’ ESG performance.

Second, improving environmental protection regulations and market mechanisms, with a focus on strengthening “end-treatment” is crucial. The government can introduce stricter pollutant emission standards and resource-use efficiency requirements, compelling resource-based enterprises to enhance their end-treatment capabilities and upgrade their environmental protection technologies. Additionally, the government can require enterprises to regularly disclose information on environmental protection investments, pollutant emissions, and resource-use efficiency, thereby enhancing the transparency and credibility of environmental governance.

Third, promoting green technological innovation and enhancing “front-prevention” capabilities are equally important. The government can establish special research and development (R&D) funds for green technologies to encourage resource-based enterprises to invest in developing clean production processes, circular economy models, etc., thereby reducing resource consumption and pollution emissions from the source. Simultaneously, the government can formulate supportive policies for the promotion and application of green technologies, such as tax incentives, subsidies, or preferential government procurement policies, to facilitate the rapid implementation and widespread application of green technologies.

Fourth, making differentiated decisions based on enterprise characteristics to strengthen the enhancing effect of ESG peer effects. For proactive enterprises with strong self-improvement motivations, technical guidance, financial support, and policy incentives can be provided to further strengthen their internal driving forces. For passive enterprises that rely on external pressures, stricter supervision, higher standards, or demonstration cases can be used to prompt them to actively respond to peer effects and improve their ESG performance. Moreover, the government should strengthen the supervision and guidance of key enterprises in the supply chain to ensure they play a leading role in the peer effects of ESG performance.

While the findings offer novel insights, the study also has several limitations. First, the sample has limitations. This study selects resource-based enterprises listed on China’s A-share market, resulting in a relatively narrow sample scope. Future research can expand the sample to include enterprises from different industries, of varying sizes, and located in different countries and regions. This will allow for an in-depth examination of the differences and commonalities in the peer effects of ESG performance across different contexts, providing more universally applicable references and guidance.

Second, this paper does not account for all potential influencing factors. Although this study considers factors such as improvement motivations, supply chain discourse power, and driving networks in relation to their impact on the peer effects of ESG performance, there may be other relevant factors in the actual economic environment. Future research can conduct a more comprehensive analysis to build a more robust theoretical framework that more accurately explains the formation mechanisms and pathways through which corporate ESG peer effects operate.

DECLARATIONS

Authors’ contributions

Writing - original draft, visualization, software, methodology, investigation, formal analysis, data curation, conceptualization: Yu, Z.

Writing - review and editing, validation, investigation, funding acquisition: Xu, D.

Writing - review and editing, validation, supervision, project administration, investigation: Dou, S.

Writing - review and editing, validation, supervision, resources, project administration, funding acquisition, conceptualization: Zhu, Y.

Availability of data and materials

Data in this study are available from the corresponding author upon reasonable request.

Financial support and sponsorship

This research was funded by National Science and Technology Major Project of the Ministry of Science and Technology of China (2024ZD1002002), National Natural Science Foundation of China (42572386; 72204235; 72504263; 72573163), China Postdoctoral Science Foundation (2022M722948; 2025T181019).

Conflicts of interest

All authors declared that there are no conflicts of interest.

Ethical approval and consent to participate

Not applicable.

Consent for publication

Not applicable.

Copyright

© The Author(s) 2025.

REFERENCES

1. Friede, G.; Busch, T.; Bassen, A. ESG and financial performance: aggregated evidence from more than 2000 empirical studies. J. Sustain. Finance. Invest. 2015, 5, 210-33.

2. Luo, X.; Xiao, J.; Zhou, J. Is green contagious? -Local peer effects of corporate green investment. Int. Rev. Econ. Finance. 2025, 104, 104650.

3. Ali-rind, A.; Boubaker, S.; Jarjir, S. L. Peer effects in financial economics: a literature survey. Res. Int. Bus. Finance. 2023, 64, 101873.

4. Tao, F.; Wang, X.; Xu, Y.; Zhu, P. Digital transformation, resilience of industrial chain and supply chain, and enterprise productivity. China. Ind. Econ. 2023, 5, 118-36.

5. Dong, Y.; Li, D.; Ma, P.; Choi, Y. Investee peer effect on firm Innovation: an uncertainty-reduction perspective. Technovation 2025, 146, 103291.

6. Sun, P.; Liu, Y.; Jiang, D. Peer effect of OFDI decision-making on corporate trade networks. J. World. Econ. 2022, 45, 58-83.

7. Lian, Y.; Ye, T.; Zhang, Y.; Zhang, L. How does corporate ESG performance affect bond credit spreads: empirical evidence from China. Int. Rev. Econ. Finance. 2023, 85, 352-71.

8. Yan, R.; Jiang, X. Customer enterprises’ ESG rating and supplier enterprises’ green innovation. Syst. Eng. Theory. Pract. 2025, 45, 1168-88.

9. Li, Q.; Wang, R.; Shi, Z. Spillover effect of “chain master” firms’ ESG performance. J. Zhongnan. Univ. Econ. Law. 2024, 5, 138-49.

10. Li, J.; Lian, G.; Xu, A. How do ESG affect the spillover of green innovation among peer firms? Mechanism discussion and performance study. J. Bus. Res. 2023, 158, 113648.

11. Li, Z.; Li, Z. Research on peer effect of enterprise ESG information disclosure. Nankai. Bus. Rev. 2023, 26, 126-38. https://nbr.nankai.edu.cn/nkglpl/article/abstract/220922006?utm_source (accessed 2025-11-17).

12. Tian, J.; Li, T.; Yang, X. Environmental regulation intensity and ESG rating quality. Rev. Econ. Manag. 2024, 40, 58-69.

13. Chen, Y.; Liu, D.; He, H.; Li, L. Peer effects of ESG greenwashing within board networks. Int. Rev. Financ. Anal. 2025, 106, 104540.

14. Yuan, P.; Ren, Y.; Dong, X. Mentors and benefactors: regional peer effects on corporate ESG performance. J. Chongqing. Univ. (Soc. Sci. Ed). 2025, 31, 76-95.

15. Xie, X.; Luo, D.; Gao, Y. Collaborative mechanism of supply chain enterprises based on green innovation: an empirical study. J. Ind. Eng. Eng. Manag. 2019, 33, 116-24.

16. Yu, Y.; Choi, Y. Stakeholder pressure and CSR adoption: the mediating role of organizational culture for Chinese companies. Soc. Sci. J. 2016, 53, 226-34.

17. Yan, B.; Cheng, M.; Wang, N. ESG green spillover, supply chain transmission and corporate green innovation. Econ. Res. J. 2024, 7, 74-93. https://kns.cnki.net/nzkhtml/xmlRead/trialRead.html?dbCode=CJFD&tableName=CJFDTOTAL&fileName=JJYJ202407005&fileSourceType=1&appId=KNS_BASIC_PSMC&invoice=MyFGS/b/Zhq0j4pDj9Y9DT4PLD/2hXgfHKv0g6976igQtOoayr6iS4nCb3C/ixW3BpnpveQjMrJ3tsATvBC51YoZQzlkUO5YDViPGP62gGR8YuABmMu+L0PW8YuIOdyzcn23pLEA9vy/jqpnG8FQyhqbOMERZagwOgeuzl2Fze8= (accessed 2025-11-18).

18. Yuan, Q.; Peng, T.; Liang, J. Collaborative equity networks in the supply chain and peer effects on corporate green transition. Fin. Res. Lett. 2025, 73, 106548.

19. Schiller, C. Global supply-chain networks and corporate social responsibility. In 13th Annual Mid-Atlantic Research Conference in Finance (MARC) Paper, SSRN.

20. Dai, R.; Liang, H.; Ng, L. Socially responsible corporate customers. J. Financ. Econ. 2021, 142, 598-626.

21. Tang, J.; Wang, X.; Liu, Q. The spillover effect of customers’ ESG to suppliers. Pac. Basin. Financ. J. 2023, 78, 101947.

22. Zhang, H.; Feng, Y.; Wang, Y.; Ni, J. Peer effects in corporate financialization: the role of Fintech in financial decision making. Int. Rev. Financ. Anal. 2024, 94, 103267.

23. Leary, M. T.; Roberts, M. R. Do peer firms affect corporate financial policy? J. Finance. 2014, 69, 139-78.

24. Wang, P.; Xue, W.; Li, Z. How does peer firms’ ESG performance affect carbon emission reductions? Fin. Res. Lett. 2025, 83, 107711.

25. Liang, Z.; Yang, X. The impact of green finance on the peer effect of corporate ESG information disclosure. Fin. Res. Lett. 2024, 62, 105080.

26. Lu, R.; Wang, C.; Deng, M. “Peer effect” in capital structure of China’s listed firms. Bus. Manag. J. 2017, 39, 181-94.

27. Hu, J.; Yu, X.; Han, Y. Can ESG rating promote green transformation of enterprises? J. Quant. Technol. Econ. 2023, 40, 90-111.

28. Li, J. Research on ESG risk premium and excess returns in China’s a-share market. Secur. Mark. Herald. 2021, 6, 26-35. https://kns.cnki.net/nzkhtml/xmlRead/trialRead.html?dbCode=CJFD&tableName=CJFDTOTAL&fileName=ZQDB202106003&fileSourceType=1&appId=KNS_BASIC_PSMC&invoice=KQbrtWOsV/iTbLPOFSMe2xFlEgZpXQoitNhBVq/taJtCfmXkWrBY4tnPSGyHsspttxj6I9AA2gQQ87hYv+MLq6IYwdoioi8I5jtdc71C+jJwYEyy0Z6Ao5Qww/VwlSp8WjyNVoA35nGxDsEP6mPweRumszBkrZsPFDsyYBJyrNo= (accessed 2025-11-18).

29. Gao, Y.; Liu, S.; Yang, L. The dynamics of peer influence in corporate ESG practices. Int. Rev. Financ. Anal. 2025, 103, 104186.

30. Khoo, J.; Cheung, A. K. Firms’ organisation capital: do peers matter? Int. Rev. Financ. Anal. 2024, 96, 103619.

31. Ding, Q.; Huang, J.; Chen, J.; Wang, D. ESG peer effects and corporate financial distress: an executive social network perspective. Int. J. Fin. Econ. 2025, 30, 2284-310.

32. Zheng, H.; Shi, X.; Deng, X. A study on the industry peer effects in enterprise digital transformation. Contemp. Financ. Econ. 2025, 3, 98-111.

33. Lin, Z.; Wei, W. Does ESG performance contribute to reducing customer concentration? J. Anhui. Univ. (Philos. Soc. Sci. Ed). 2023, 47, 121-32.

34. Li, Y.; Wu, Y.; Tian, X. Enterprise ESG performance and supply chain discourse power. J. Financ. Econ. 2023, 49, 153-68.

35. Ding, Q.; Huang, J.; Chen, J. Does digital finance matter for corporate green investment? Evidence from heavily polluting industries in China. Energy. Econ. , 2023,117,106476.

36. Ma, D.; Wang, M.; Zeng, B.; Jiang, H. Peer effects of firm environmental protection expenditures. Fin. Res. Lett. 2024, 65, 105493.

37. Li, Y.; Niu, H.; Xu, H. Those who are close to vermilion are red: can customers included in the carbon emissions trading pilot affect corporate ESG performance? R&D. Manag. 2024, 36, 40-52.

38. Li, W.; Zhang, Y.; Zheng, M.; Li, X.; Cui, G.; Li, H. Research on green governance and its evaluation of Chinese listed companies. J. Manag. World. 2019, 35, 126-133+160.

39. Xiao, R.; Ma, B.; Qian, L.; Shen, J. Impact of the low-carbon city pilot policy on corporate green innovation and its mechanisms. China. Popul. Resour. Environ. 2023, 5, 127-39. https://kns.cnki.net/nzkhtml/xmlRead/trialRead.html?dbCode=CJFD&tableName=CJFDTOTAL&fileName=ZGRZ202305011&fileSourceType=1&appId=KNS_BASIC_PSMC&invoice=vxDM5WtST1wuhqHIlKOPnqCCslNSTYHTrOx7XActBURWG8B/I3Bz0/HOaOfJTuB3BzBR74/7oPyo9MRTMIshfpb4TSL0D3QCqsO8HD/jwwSI8tHdT5+vSJ9SmvdOHfWCc0Z9BJm1RPtHBCBSQpT5bCc49h7WSVLnzl3TV2eaWvY= (accessed 2025-11-18).

40. Ren, X.; Zeng, G.; Sun, X. The peer effect of digital transformation and corporate environmental performance: empirical evidence from listed companies in China. Econ. Model. 2023, 128, 106515.

41. Adhikari, B. K.; Agrawal, A. Peer influence on payout policies. J. Corp. Finance. 2018, 48, 615-37.

42. Jiang, T. Mediating Effects and Moderating Effects in Causal Inference. China. Ind. Econ. 2022, 5, 100-20.

Cite This Article

How to Cite

Download Citation

Export Citation File:

Type of Import

Tips on Downloading Citation

Citation Manager File Format

Type of Import

Direct Import: When the Direct Import option is selected (the default state), a dialogue box will give you the option to Save or Open the downloaded citation data. Choosing Open will either launch your citation manager or give you a choice of applications with which to use the metadata. The Save option saves the file locally for later use.

Indirect Import: When the Indirect Import option is selected, the metadata is displayed and may be copied and pasted as needed.

About This Article

Copyright

Data & Comments

Data

0

Comments

Comments must be written in English. Spam, offensive content, impersonation, and private information will not be permitted. If any comment is reported and identified as inappropriate content by OAE staff, the comment will be removed without notice. If you have any queries or need any help, please contact us at [email protected].