Critical review: a standardized blueprint for green certificate integration in life cycle assessment

0

0 Abstract

Green certificates (GCs), such as guarantees of origin (GOs), support renewable electricity tracking and corporate greenhouse gas reporting, but methodological inconsistencies, particularly in life cycle assessment (LCA) applications, undermine their credibility, transparency, and environmental benefits. This review critically evaluates current GC practices and their integration into LCA frameworks, identifying key challenges including double counting, insufficient geographic and temporal matching, and emission reallocation effects in residual electricity mixes. The review first examines global GC trading systems and associated policies, highlighting structural differences across regions such as the European Union, the United States, and China. It then explores how GCs are treated in market- and location-based accounting approaches for Scope 2 emissions. A multi-stage standardization framework is proposed, encompassing GC generation, trade, allocation, and application in LCA. Particular emphasis is placed on the need for harmonized certificate types, data traceability, and temporal alignment between energy use and certificate validity. Finally, policy and regulatory recommendations are presented to strengthen oversight, improve the reliability of market mechanisms, and foster international collaboration. This includes a call for reform in key protocols and a shift toward more granular, transparent tracking systems. The findings support more accurate environmental claims and promote a credible, standardized use of GCs in LCA and sustainability reporting.

Keywords

INTRODUCTION

With the rapid development of human society in the past century, climate change, as a global environmental issue, has also attracted increasing attention. The Paris Climate Conference set a goal to limit the global average temperature increase to within 2 °C above pre-industrial levels, with an aspirational target of 1.5 °C. Achieving this requires keeping cumulative global Carbon Dioxide (CO2) emissions below 1 trillion tons and reducing global Greenhouse Gas (GHG) emissions by 40%-70% by 2050 compared to 2010 levels, to reach zero emissions by the end of the century[1]. Achieving GHG neutrality involves two main strategies: decarbonization and defossilization. Decarbonization involves eliminating carbon use across industries, especially in energy conversion. Over 90% of national GHG emissions originate from fossil energy conversion in sectors like industrial production, transportation, and households[2]. It is evident that fossil fuels still dominate total electricity production[3,4]. However, renewable energy, particularly wind and solar power, is rapidly increasing and entering a significant growth phase.

Given the central role of electricity in powering economic activities, reducing CO2 emissions from electricity generation is a highly effective strategy for mitigating GHG emissions. Consequently, the power industry has been actively working to lower its CO2 emissions by adopting renewable energy sources such as solar power and hydropower[5]. Except for the very minimal emissions that occur during plant construction and maintenance, renewable energy sources like solar, wind, hydro, and geothermal power have no emissions associated with their generation per megawatt-hour (MWh). However, what cannot be ignored is that it does have emissions for generating renewable energy from burning biomass; the amount varies depending on the fuel types, processing methods, and application[6]. To accelerate the process, the Tradable Green Certificate (TGC) is introduced to provide additional revenue to ensure a baseline level of renewable energy production. By applying Green Certificates (GCs), there are several advantages: (1) they can be traded internationally and align with public support schemes; (2) they bypass physical limitations of electricity transfer; and (3) they decouple the timing of supply and demand for rebound effects[7].

Moreover, energy markets are plagued by information asymmetries, as end users typically lack transparent, verifiable data to distinguish renewable‐sourced electricity from fossil‐based supply. As electrons are indistinguishable, when using a common electrical grid, electrons from various generators are combined together. This can lead to adverse selection, where those wanting renewable energy may not buy it at all[8]. With GCs, it helps by providing information about the energy's origin, allowing consumers to make informed choices. For example, the introduction of GOs - the EU’s most prevalent form of GC - provides a verifiable tracking mechanism that distinguishes renewable electricity covered by GOs from conventional grid supply. Additionally, beyond serving as a tracking mechanism, GOs also establish enforceable contractual claims between supplier and customer - specifying the generation facility, energy source, production date range, and more. In effect, GOs empower consumers to choose a tailored electricity mix, rather than passively accepting the traditional, geographically determined “average” grid blend that depends solely on local generation and cross-border flows.

LCA, as a tool for systematically evaluating environmental sustainability, directly reflects the environmental impacts and performance of products or organizations. When considering input indicators and data in LCA, energy consumption - whether from upstream, production, or downstream processes - must be accounted for. As more corporations or individuals adopt clean energy to meet sustainability standards or criteria, GCs cannot be ignored as proof of the green electricity generation, trade, and usage. Since LCA requires the calculation of all different types of energy within its scope, it includes the portion of renewable energy certified by GCs. Integrating GCs into LCA could enhance the credibility and comprehensiveness of environmental impact assessments by providing verified data on environmental performance. Moreover, this integration demonstrates commitment to low-carbon economies, facilitates accurate GHG emission inventories, and supports the assessment of green processes and products[9]. By better reflecting the environmental benefits of renewable energy, it could also lead to improved informed decision making and sustainability evaluation[10].

As companies - whether by regulatory requirement or voluntary commitment - purchase GCs to bolster their environmental profile, GC data must be integrated into Life Cycle Assessment (LCA)’s electricity-use module to accurately interpret the resulting product or service impacts[11]. However, few studies in the existing literature have systematically examined the integration of GCs into LCA or identified the associated challenges, which is an essential step for advancing their effective use. Therefore, this review mainly focuses on identifying the limitations of using GCs in LCA and proposing standards for their appropriate use. Given the previous introduction, the main research questions in this study are: (1) What are the limitations for the application of GCs in LCA? (2) How should the GCs be applied in the LCA of products, services, and companies? It should also be noted that in this article, most of the cases and examples provided are of GOs; nevertheless, this does not affect the goals and results of the research.

ELEVATING GCs THROUGH LCA

Focusing on two key aspects - GC and LCA, this section adopts a staged and thematic literature review approach. It begins with conceptual foundations and progressively narrows its scope toward the intersection between the application of GCs and LCA. Specifically, it traces the evolution of GC typologies, investigates relevant tradable GC markets and the role of GCs in electricity-based carbon emission disclosure, reviews the application of LCA in environmental assessment, and explores the GC-LCA nexus in depth. In more detail, GOs are presented as a representative example of GCs particularly within the context of relevant legislation and regulatory frameworks. The life cycle of GCs in electricity disclosure and the fundamental modeling approach of the LCA approach are also discussed. Finally, by linking LCA with Scope 2 emissions, the GC-LCA intersection is illustrated, underscoring the urgency of addressing these cross-cutting issues to foster the development of renewables and promote sustainability.

Critical evolution of GC typologies

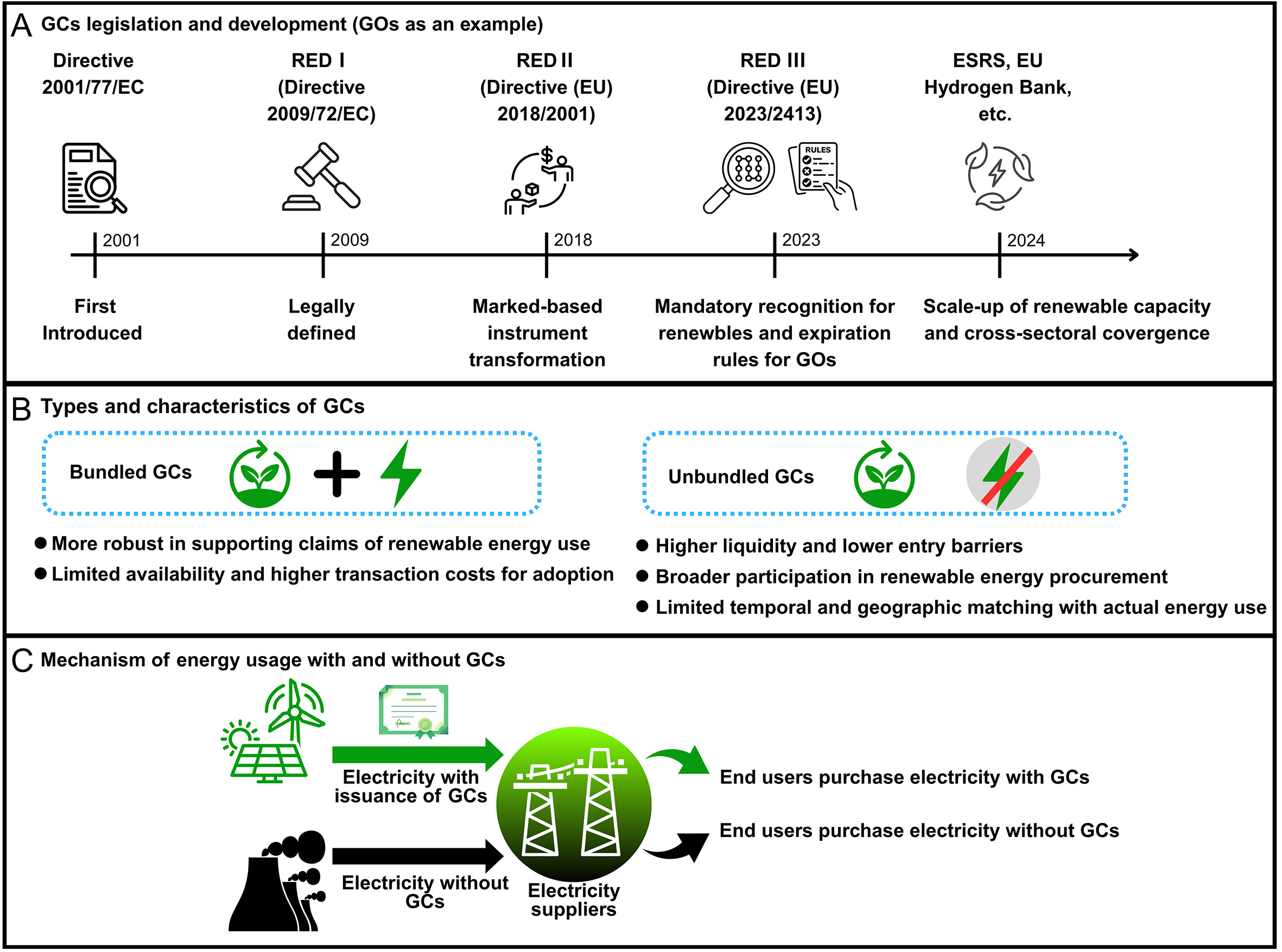

GCs serve as a widely adopted mechanism for achieving national renewable energy targets, incentivizing market-based transitions toward low-carbon electricity systems[12-14]. Their terminology varies by jurisdiction: Renewable Energy Certificates in the United States, Renewable Energy Credits for Voluntary Purchases in Canada, Renewable Obligation Certificates in the United Kingdom, and GOs in the European Union and other European countries. For every MWh of verified renewable electricity generation, registered producers receive a GC. Once entered into national or regional registries, these certificates can be traded as commodities representing the environmental benefits of producing electricity from renewable sources, independent of the underlying physical power. Since the early 21st century, various proposals have promoted GCs as proof of the origin of electricity. As depicted in Figure 1A, the legal framework for GOs has evolved from a basic certification tool in 2001 to a core component of the EU’s market-based renewable energy governance system[15].

Figure 1. Overview of Green Certificates (GCs): (A) GCs legislation and development; (B) types and characteristics of GCs; and (C) mechanism of energy usage with and without GCs. The icon was created via www.canva.com.

First introduced under Directive 2001/77/EC (the 1st Energy Package), GOs were initially conceived as informational tools to verify renewable electricity generation[16]. Their role was clarified with the adoption of the 2009 Renewable Energy Directive (RED I), which defined them as electronic attestations confirming the renewable origin of a specified energy quantity[17]. At that stage, GOs were still largely confined to national registries, with limited market functionality. A major regulatory shift occurred with the Clean Energy for All Europeans Package through the RED II Directive (2018/2001/EU), which explicitly authorized the transfer of GOs and transformed them from static labels into market-based instruments[18]. RED II also laid the foundation for standardized issuance, mutual recognition across borders, and integration of non-electricity energy carriers such as green gases and renewable heating and cooling.

This trajectory continued with the Fit-for-55 Package and the RED III Directive (2023), which introduced further refinements[19,20], including mandatory recognition of GOs for all renewable fuels [e.g., renewable fuels of non-biological origin (RFNBOs)], simplified issuance for small-scale producers, expiration rules to prevent stockpiling and double counting, and improved temporal and geographic granularity. Importantly, RED III also aligned GOs with EU climate objectives, notably the 55% emissions reduction target by 2030 under the European Green Deal, establishing them as central instruments in market-based accounting under frameworks such as the Corporate Sustainability Reporting Directive (CSRD), which mandates dual Scope 2 accounting and recognizes GOs and PPAs for emissions tracking[21]. In 2024 and beyond, subsequent regulatory innovations - including the European Sustainability Reporting Standards (ESRS) framework, “Renewables Acceleration Areas”, and hydrogen certification schemes integrating GOs - further reinforce their role across sectors[22,23]. Collectively, these developments reflect the EU’s shift from administrative attestations to market-embedded, multifunctional instruments that support environmental accountability, investment facilitation, and scalable, climate-neutral energy governance.

Beyond geographic distinctions by issuing authorities, GCs can be commonly categorized based on their association with electricity delivery into bundled and unbundled types, with differing implications for credibility, traceability, and market alignment[24]. According to Figure 1B, bundled GCs refer to certificates sold in conjunction with the physical delivery of renewable electricity, providing a high-integrity link between consumption and generation, and are considered more robust for verifiable corporate sustainability claims under frameworks such as the GHG Protocol, Carbon Disclosure Project (CDP), or RE100 commitments[25-27]. By contrast, unbundled GCs are traded independently of electricity supply, enhancing market liquidity and accessibility but raising concerns regarding temporal and geographic disconnection, double counting, lack of additionality, and greenwashing. This dual structure highlights a fundamental tension between market accessibility and environmental integrity. Conversely, while bundled GCs offer stronger alignment with principles of environmental additionality and traceable impact, their limited availability and higher transaction costs may hinder widespread adoption. Therefore, emerging regulatory frameworks - such as the EU’s CSRD and the revision of the Energy Taxation Directive - are expected to strengthen disclosure and verification standards, suggesting a potential convergence toward high-integrity instruments, favoring bundled or hybrid models with stricter temporal and locational matching[21,28]. A reassessment of GC design, reporting, and verification mechanisms is thus essential for maintaining system legitimacy in evolving energy governance.

Figure 1C illustrates the operational mechanism of electricity consumption with and without the integration of GCs, highlighting the structural bifurcation introduced by market-based renewable energy certification systems. GCs distinguish renewable from conventional electricity via tradable certificates rather than physical separation, enabling consumers to make verifiable claims about energy sourcing. Suppliers aggregate multiple sources, and renewable producers receive GCs that can be sold bundled with the electricity or separately. While bundled GCs link consumption to generation, unbundled GCs enhance market liquidity but may lack temporal and spatial correlation, raising concerns over additionality, fungibility, and accountability. This bifurcated model internalizes environmental attributes into energy markets, yet challenges accurate decarbonization tracking. As the market for GCs matures, ensuring robust traceability, standardization, and alignment with actual grid decarbonization remains critical to maintaining the integrity and efficacy of the system.

GCs in TGC markets and electricity disclosure

According to Amundsen and Bergman, Sweden introduced a TGC market in 2003 as a market-based mechanism to stimulate investments in renewable electricity generation[13]. Unlike direct governmental subsidies, the TGC system seeks to internalize the cost of renewable energy deployment through market incentives. Under this system, electricity producers receive one certificate per MWh of green electricity generated, which can be traded on the market immediately or stored for future sale. On the demand side, electricity consumers - particularly retailers and large-scale users - are mandated to purchase a specific share of TGCs proportional to their total electricity consumption, thereby ensuring continued demand for the certificates and creating a self-sustaining price mechanism driven by supply-demand dynamics. While Sweden’s approach exemplifies the potential of TGCs to mobilize private investments without fiscal burdens on the state, the market’s long-term efficiency and fairness depend on regulatory oversight, price stability, and the credible verification of green electricity generation. At the European level, efforts to harmonize such mechanisms are evident in the development of the European Energy Certificate System (EECS), coordinated by the Association of Issuing Bodies (AIB)[29]. The EECS provides a standardized framework for the issuance, transfer, and cancellation of GOs, thus enhancing transparency and interoperability across national energy certificate markets. However, challenges remain in aligning certificate systems across jurisdictions, preventing double counting, and ensuring the environmental additionality of the renewable electricity represented by these certificates. These issues warrant further scrutiny, particularly when GCs are considered in environmental accounting or integrated into LCA frameworks.

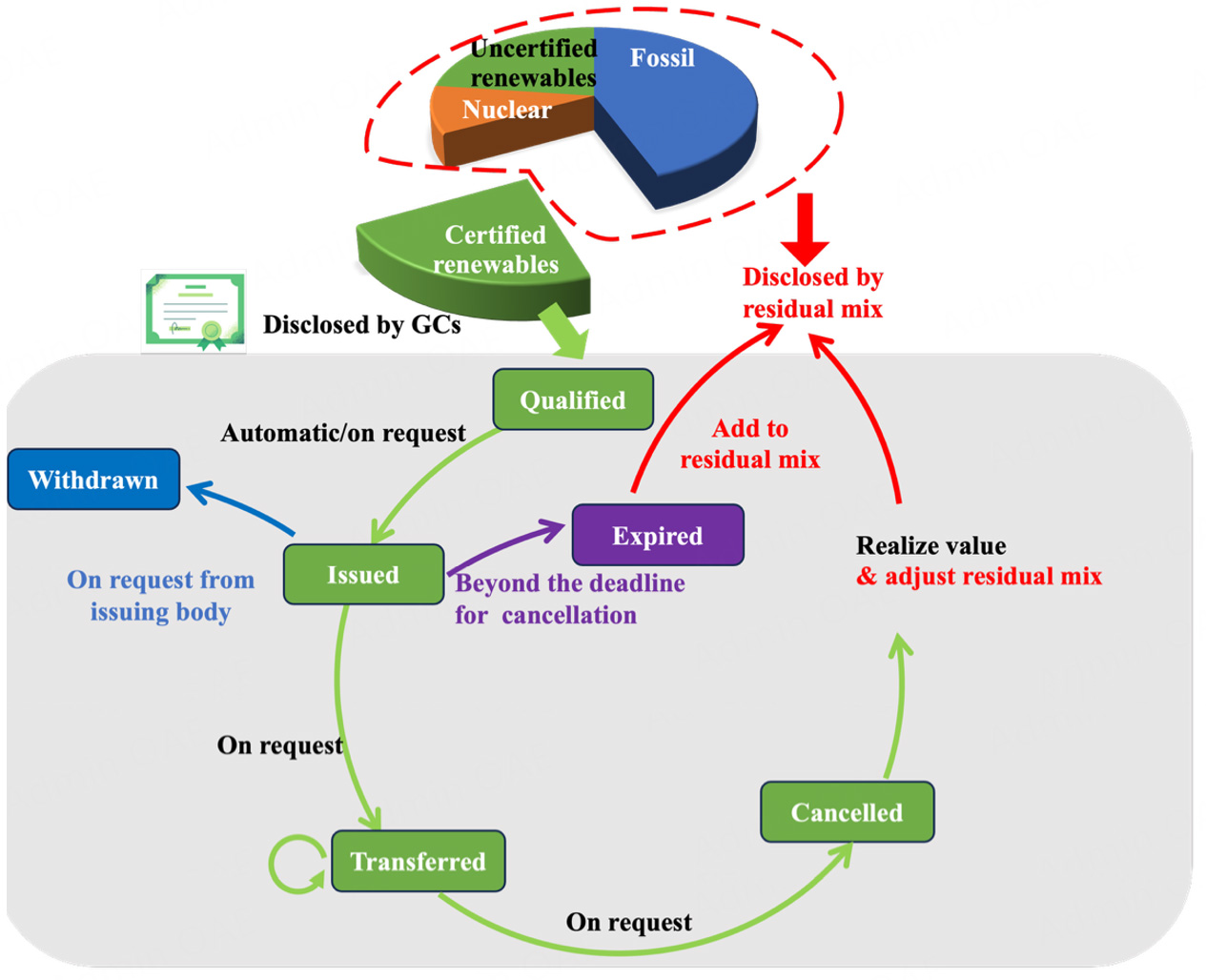

Figure 2 depicts the dynamic life cycle of energy certificates, illustrating their progression through key operational states: Qualified, Issued, Transferred, and Cancelled. Two additional terminal states are also represented: Expired, which automatically applies to certificates that have not been cancelled within a defined time frame (typically one year), and Withdrawn, which accounts for certificates issued in error. Specifically, the issuing body (i.e., authorized entity responsible for the issuance and management of GCs) can request the withdrawal of issued certificates when irregularities, administrative errors, or compliance violations are detected. The transitions between these states (e.g., from Issued to Transferred and subsequently Cancelled) reflect the administrative and commercial processes that ensure traceability and compliance within certificate-based renewable energy schemes. Additionally, Figure 2 complements this by highlighting the role of GCs in electricity disclosure practices. According to the Electricity Market Directive[30], suppliers are required to disclose not only the source of electricity (renewables, fossil, nuclear) but also its environmental implications (e.g., CO2 emissions, radioactive waste). The figure demonstrates that consumers can voluntarily purchase GCs to attribute renewable qualities to their electricity consumption, thereby enhancing the transparency and perceived sustainability of their energy use. Meanwhile, users without GCs rely on the Residual Mix, which aggregates non-traceable electricity sources and typically reflects a higher share of fossil and nuclear energy. This dual system of disclosure underscores the market-based differentiation enabled by GCs and the regulatory role of residual mix accounting.

Figure 2. Life cycle of a GC for electricity disclosure. Very small parts of this figure were adapted from Ref.[29], but have been substantially redrawn and integrated with the authors’ own concepts. All original sources are properly acknowledged in the figure legend. (Note that certified renewables refer to the share of renewable energy certified by GCs, whereas uncertified renewables denote those not officially certified by GCs, and are included in the residual mix).

Application of LCA in environmental assessment systems

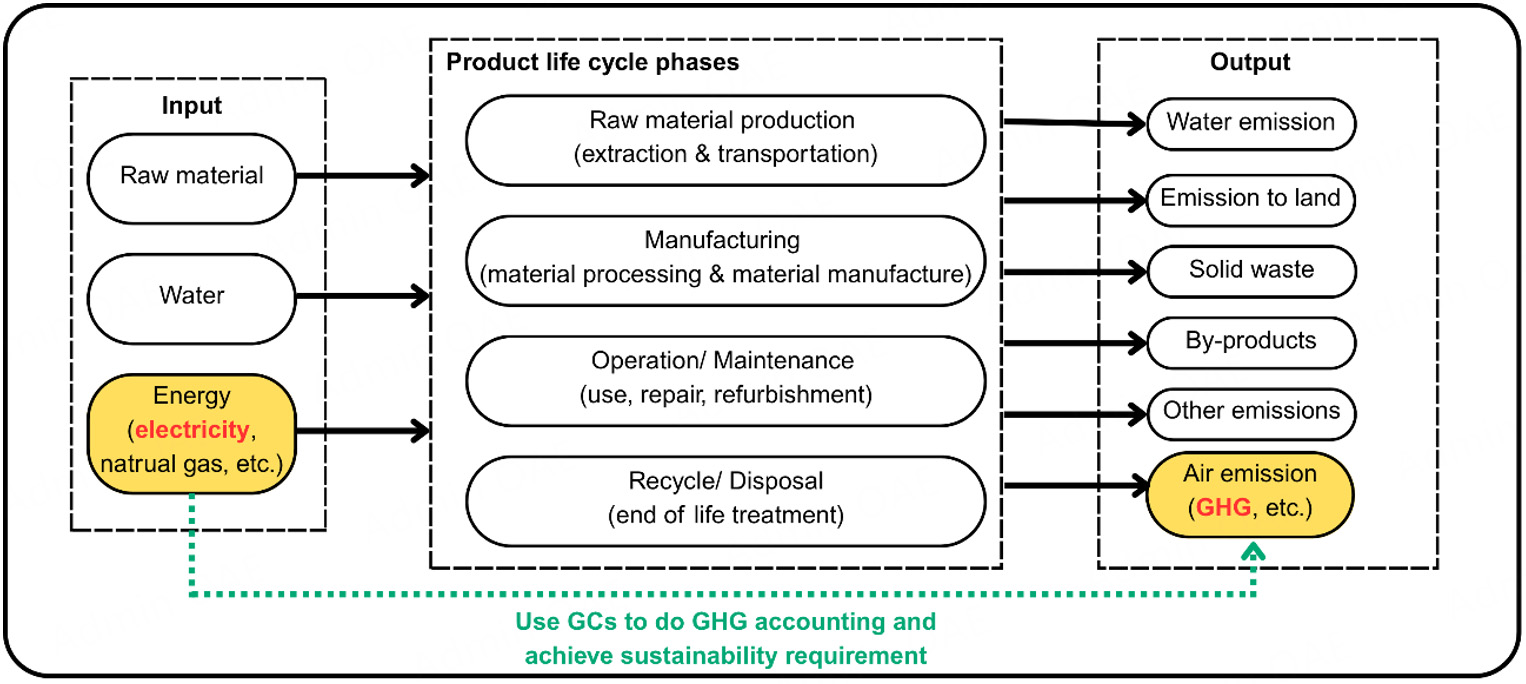

LCA is a structured and widely recognized tool for evaluating the environmental performance of a product, service, or process across all life cycle stages - from raw material extraction through production, use, and end of life[31,32]. As shown in Figure 3, it accounts for all relevant inputs (e.g., energy, water, materials) and outputs (e.g., emissions, waste), offering a comprehensive picture of environmental interactions. The diagram illustrates the product life cycle, emphasizing the role of energy (particularly electricity) in contributing to air emissions, including GHGs. Energy use during various phases - manufacturing, operation, and end-of-life treatment - is a significant input affecting the overall environmental impact. The highlighted feedback loop indicates that Green Certificates (GCs) can be applied to account for GHG emissions associated with energy consumption, thus supporting sustainability compliance and emission reduction strategies. This systems-based perspective is essential for identifying environmental hotspots and improving sustainability performance in both policy and business contexts[33].

Figure 3. Product life cycle phases linked to GCs and the energy disclosure system.

When applied in regulatory or market mechanisms - such as GCs or energy disclosure systems - LCA plays an increasingly supportive role. For example, electricity suppliers in the EU are required to disclose the environmental characteristics of their power mix, including CO2 emissions and radioactive waste. Here, LCA can help ensure that the information linked to electricity disclosure and GCs is based on quantifiable environmental impacts. As illustrated earlier (see Figure 2), GOs enable consumers to claim renewable attributes of electricity, while uncertified renewables are covered by the Residual Mix. These disclosure mechanisms, though accounting-oriented, could be further strengthened when supported by LCA data - offering more consistent and credible environmental profiles for both certified and residual electricity.

In this context, the modeling approach chosen for LCA becomes crucial. As outlined in Table 1, there are two main types[32-34]:

Extensive conclusion for the three LCA modeling approaches[34]

| Aspect of comparison | Consequential approach | Attributional approach | |

| Decision support | Decision support | Accounting | |

| Aim | Analyze what impact a decision has on the environment | Assess a product/service environmental profile | Assess a product/service environmental profile |

| Purpose | Meso/macro-level decision support | Micro-level decision support | Accounting/reporting |

| Time | Past/future | Past/future | Past/future |

| Relations | Established through models of general equilibrium | Physical, financial, or contractual | Physical, financial, or contractual |

| Environment impacts | Caused by a decision's effects | Caused by the physical, financial, and/or contractual interactions among product systems | Caused by the physical, financial, and/or contractual interactions among product systems |

| Affected background processes/technologies | Large-scale technologies/processes impacted | Small- or non-scale technologies/processes impacted | Small- or non-scale technologies/processes impacted |

• The attributional approach focuses on describing the average environmental impacts directly linked to a product or service. This makes it particularly suitable for certification systems like GCs, where clear, traceable, and standardized results are needed to inform environmental claims or labels.

• The consequential approach, on the other hand, considers the broader system-level impacts that result from changes in demand, policy, or production choices. This makes it more relevant for evaluating how GCs or similar market instruments influence the energy system over time - such as incentivizing new renewable capacity or shifting grid dynamics.

Thus, attributional LCA provides the methodological foundation for tracking and disclosing environmental attributes of electricity, while consequential LCA offers insights into the strategic and long-term impacts of implementing or reforming GC schemes. Understanding this distinction ensures that LCA is applied appropriately in environmental governance and market mechanisms. While both approaches are valid, their use should match the specific purpose - whether it is verifying environmental performance (e.g., for disclosure or reporting) or assessing broader sustainability outcomes (e.g., for investment or policy decisions).

Critical synthesis: challenges at the GC-LCA nexus

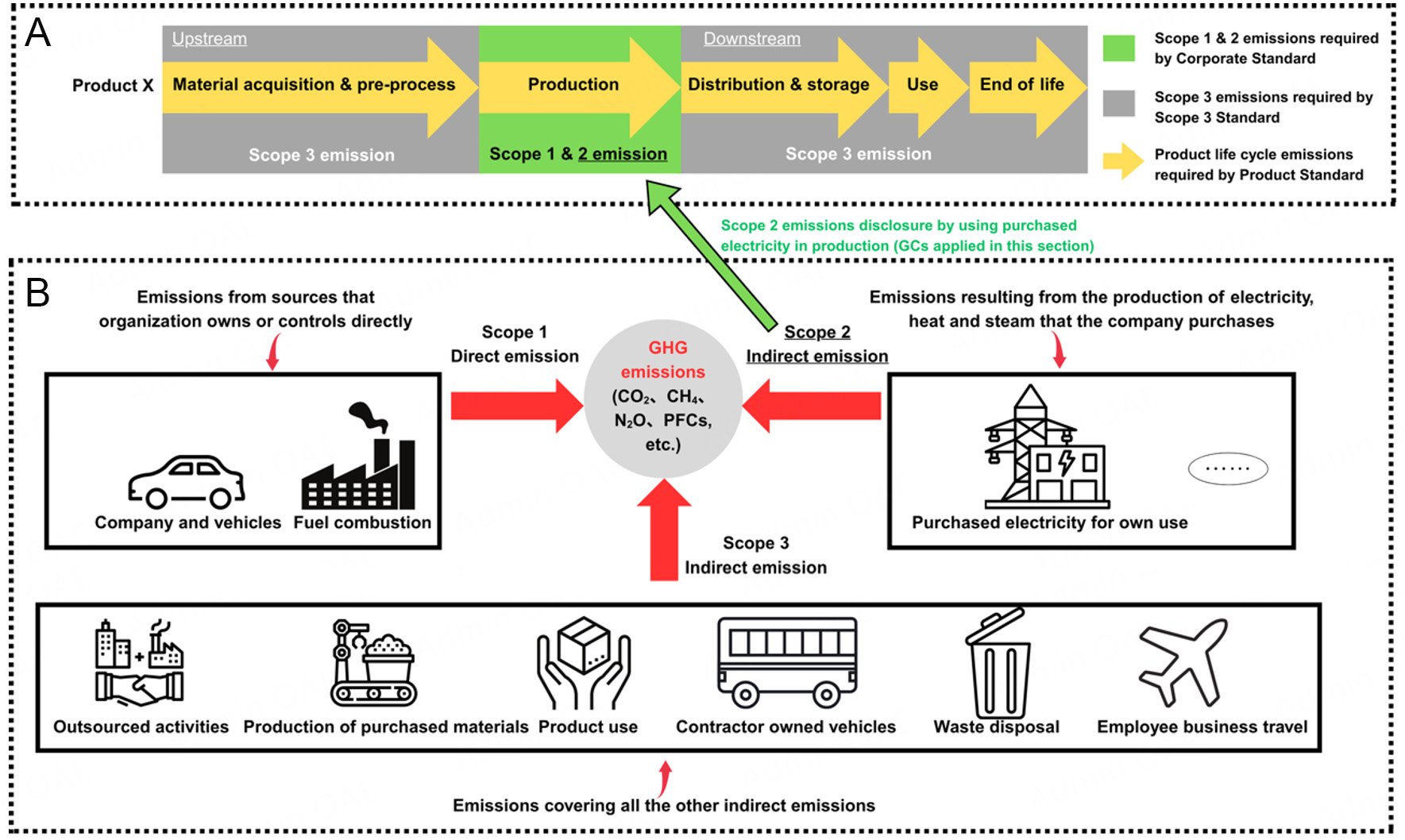

In environmental assessments of products or corporate operations, electricity consumption frequently constitutes a major source of GHG emissions, often representing a substantial fraction of the overall carbon footprints. Within the framework of LCA, the accurate treatment of electricity-related emissions necessitates careful consideration of both the origin of the electricity and the methodological approach employed to model its environmental impacts. This consideration is critical in the context of interconnected electricity grids, where the physical origin of electrons is not traceable, and where electricity from multiple generation sources is aggregated and distributed across wide geographic areas. According to the GHG Protocol[35], emissions associated with electricity consumption are categorized under Scope 2, which encompasses indirect emissions resulting from the generation of purchased electricity, steam, or heat. As illustrated in Figure 4, Scope 2 therefore occupies an intermediate position between Scope 1, which accounts for direct emissions from owned or controlled sources, and Scope 3, which captures emissions across the broader value chain, highlighting Scope 2 as a critical focus for companies aiming to manage and mitigate their climate impacts. Given that the electricity use often constitutes a significant portion of a product’s total environmental burden, rigorous accounting of Scope 2 emissions is essential to ensure the credibility and robustness of LCA results, particularly in comparative or product-level assessments intended to inform sustainable decision making.

Figure 4. Overview of how GHG emission scopes align with Corporate, Scope 3, and Product Standards (A), and how these scopes are distributed across a product’s value chain (B). Very small parts of this figure were adapted from Ref.[35], but have been substantially redrawn and integrated with the authors’ own concepts. All original sources are properly acknowledged in the figure legend. The icon was created via www.canva.com.

In practical LCA applications, four principal approaches are commonly adopted to quantify electricity-related emissions. The first approach relies on the average grid mix, which reflects the national or continental electricity generation portfolio, such as the European Network of Transmission System Operators for Electricity (ENTSO-E) database for Europe, and provides an aggregate emission factor that represents typical generation conditions. The second approach, applying the regional or local mix, accounts for spatial variations in electricity generation by considering the specific composition of nearby power plants, thereby introducing greater geographic specificity. The third approach employs the consumption mix, incorporating both domestic generation and imported electricity, thereby reflecting the combined effect of locally produced and externally sourced power. The fourth approach, based on the supplier-specific mix, becomes particularly relevant when electricity procurement is accompanied by GCs such as GOs, which certify the renewable nature of the purchased electricity[35-37]. Unlike the other approaches, the fourth approach is most relevant in attributional LCA, where GCs are used not just as proof of renewable sourcing, but also to define the specific emissions factor of the purchased electricity. This enables emission calculations to reflect the certified environmental performance of a particular energy product. Consequently, the integration of GCs into LCA modeling strengthens the reliability of Scope 2 emission accounting, supports robust comparative analyses, and enhances the transparency and traceability of corporate environmental claims.

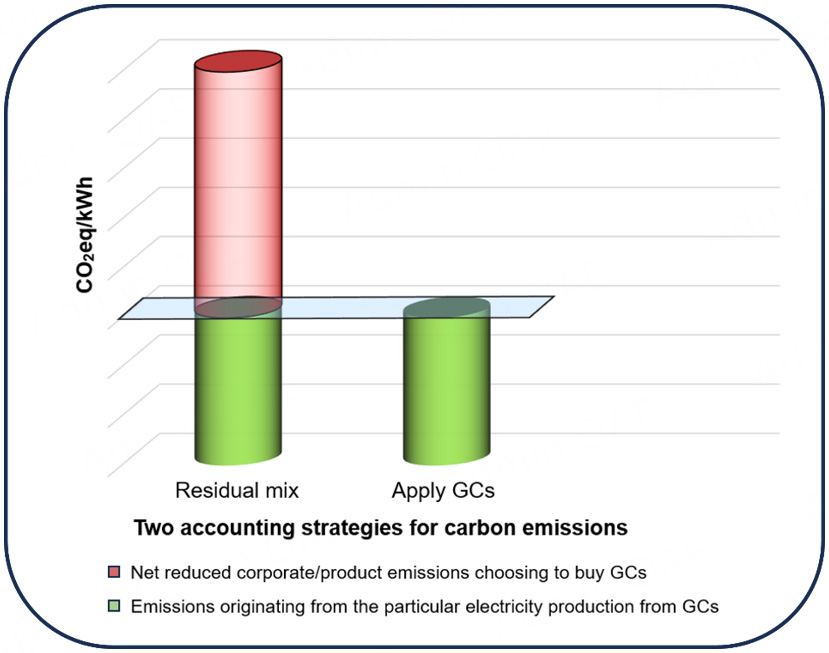

A growing and increasingly significant application of green certificates (GCs) within the framework of life cycle assessment (LCA) lies in their role as instruments for environmental benefit allocation, renewable energy intensity indicators, product environmental declarations, eco-labeling schemes, and corporate sustainability reporting. In these contexts, GCs serve as a contractual and accounting mechanism that links electricity procurement decisions to downstream environmental assessments and external communication. This linkage improves the internal consistency of environmental accounting practices and enhances the credibility of claims made by organizations regarding renewable energy use and related environmental benefits. By formally integrating GCs into LCA-based studies, companies and product systems can better align with international standards of carbon disclosure and sustainability performance reporting. Figure 5 illustrates two accounting strategies for carbon emissions associated with electricity use. The left column (“Residual mix”) represents electricity supplied directly from the general grid in the absence of GCs. It includes the average CO2-eq emissions per kWh based on the national or regional electricity mix. The green portion represents emissions already associated with existing renewable inputs in the grid, while the red portion highlights the excess emissions that could be avoided by switching to certified renewable electricity. The right column (“Apply GCs”) reflects the accounting outcome when electricity purchases are explicitly matched with GCs - typically originating from renewable sources such as wind, solar, or hydro power. Here, only the lower-impact emissions (green) from certified renewable generation are counted. The absence of the red portion in this column reflects the net emissions reduction achieved through the purchase of GCs, expressed in CO2-eq/kWh. This difference can be credited to the purchasing company or product system, aligning with attributional LCA practices and market-based accounting rules under the GHG Protocol. This figure also reinforces the idea that applying GCs offers a measurable way to reduce Scope 2 emissions, especially for organizations seeking to lower their environmental impact or make renewable energy claims. The emissions avoided through GCs can be directly incorporated into product carbon footprints, corporate disclosures, or eco-labeling schemes. Nevertheless, it is important to note that these avoided emissions represent a contractual reallocation, not necessarily a physical reduction in fossil fuel generation. For a more comprehensive understanding of the broader system-wide impacts of GC adoption - such as the extent to which certificate markets incentivize additional renewable capacity, accelerate technological deployment, or displace marginal fossil-based generation - consequential LCA provides a more suitable analytical framework. This methodological distinction is crucial to avoid overestimating the environmental benefits of GCs when evaluating long-term policy implications or energy transition scenarios.

Figure 5. Electricity-related CO2 emissions allocation using GCs vs. residual mix.

CRITICAL ISSUES IN LINKING GCs TO LCA PRACTICE

Double counting in electricity-related GHG accounting

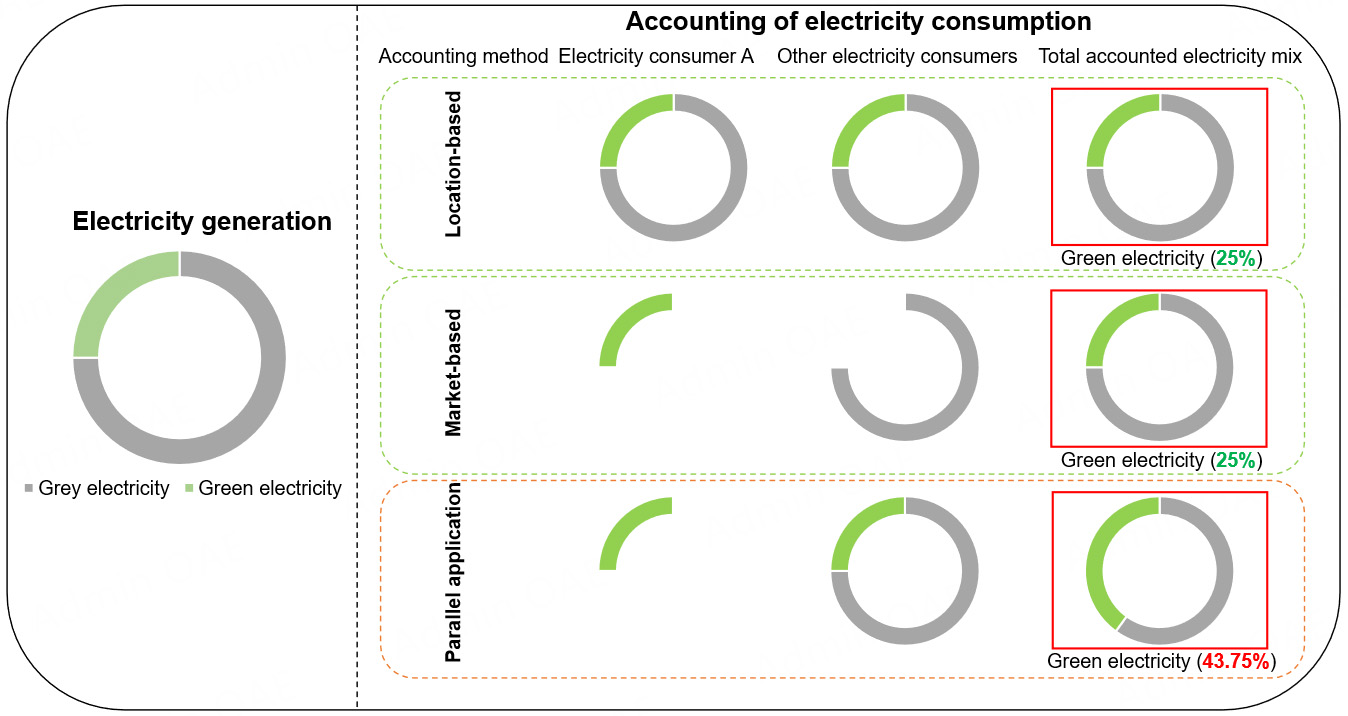

Accurately assessing the environmental impacts of electricity consumption within LCA and GHG accounting frameworks requires careful differentiation between electricity that is physically consumed and electricity that is contractually claimed via instruments such as GCs or GOs. Two dominant approaches exist for allocating GHG emissions in electricity consumption: (a) The location-based method uses average regional emission factors derived from the physical electricity mix in a defined grid area; (b) The market-based method relies on contractual instruments - such as GCs, GOs, or Renewable Energy Certificates (RECs) - to reflect specific procurement choices, often used to claim renewable attributes for Scope 2 emissions[38].

While each method is valid within its own boundary conditions, applying both methods inconsistently or simultaneously across accounting systems can lead to double counting of renewable energy benefits. This misalignment occurs when both market-based purchasers (who claim renewable electricity via certificates) and location-based users (who report based on average grid data that still includes the renewable portion) attribute the same low-carbon electricity to their consumption footprints. Figure 6 visualizes this issue using a stylized example. In a hypothetical electricity system where 25% of electricity is generated from renewable energy sources and the remaining 75% originates from conventional sources (grey electricity), inconsistencies in the application of accounting approaches can lead to substantial overreporting of renewable electricity consumption. Figure 6 illustrates this phenomenon through the case of consumer A, who consumes 25% of the total grid electricity, while the other 75% is consumed by the remaining consumers. When all consumers adopt the location-based approach, each party applies the grid’s average emission factor, which is consistent with the actual generation mix. In this case, accounting outcomes align with physical reality, as 25% of the electricity is reported as renewable and 75% as conventional. The same consistency holds when all consumers uniformly adopt the market-based approach, provided that guarantees of origin (GOs/GCs) are correctly allocated and the residual mix is adjusted accordingly. However, problems emerge when consumer A applies the market-based approach and redeems green certificates (GCs) to claim that their entire 25% electricity consumption is renewable, while other consumers simultaneously apply the location-based approach without deducting the renewable share already claimed by consumer A. Under this mixed-method scenario, consumer A accounts for 25% renewable electricity (via GCs), while the other consumers - using the unadjusted location-based grid average - still attribute 25% of their 75% share to renewables. This adds an extra 18.75%, which, when combined with consumer A’s 25% claim, yields 43.75% of total renewable electricity consumption, even though only 25% is physically generated. This discrepancy arises from the inclusion-exclusion problem in probability theory, whereby overlapping shares are effectively double-counted. The 43.75% figure thus represents a theoretical upper bound of overreporting that can occur when market-based and location-based methods are applied inconsistently within the same system[39].

Figure 6. Illustration of double counting risks from the simultaneous use of location-based and market-based electricity accounting. Very small parts of this figure were adapted from Ref.[39], but have been substantially redrawn and integrated with the authors’ own concepts. All original sources are properly acknowledged in the figure legend.

This issue is not limited to hypothetical cases. In Norway, despite 98% of electricity being produced from hydropower, only about 15% of domestic consumers purchase GOs[40]. The assumption that their electricity is already green leads to low voluntary participation. However, hydropower producers continue to sell GOs abroad - particularly to other EU countries - where they are used to substantiate renewable electricity claims. To maintain administrative coherence, Norway’s electricity mix is artificially recalibrated to reflect this export, resulting in a residual mix that misleadingly shows that Norwegians use ~50% fossil electricity. Thus, the environmental benefit of the same hydropower is double-counted: once physically in Norway and once contractually elsewhere in Europe. In North America, the problem is further complicated by the lack of a centralized, transparent registry for tracking voluntary RECs. Without exclusion mechanisms in LCI datasets (e.g., ecoinvent) to account for REC transfers, grid mixes used in LCA may unintentionally reflect both physical supply and market-based claims simultaneously. As Boguski et al. highlight, this makes it difficult to construct accurate consumption or residual mixes in the U.S. and Canada[41]. If a company uses RECs and, at the same time, applies average grid emission factors from datasets that do not exclude sold RECs, double counting inevitably arises.

This parallel application of the two accounting methods - location-based and market-based - poses serious risks to transparency, comparability, and integrity of GHG disclosures. It also undermines the environmental credibility of voluntary certificate schemes, particularly in LCA studies that aim to evaluate electricity-related Scope 2 emissions. Addressing double counting requires stronger alignment between LCA datasets, national disclosure systems, and certificate registries. Options include the explicit subtraction of claimed green electricity from residual mixes, coordinated disclosure protocols between countries (as partially implemented in Europe), and improved tracking of contractual instruments in LCI databases.

Data validity in GC-based GHG accounting

The reliability of data used in Scope 2 GHG accounting - particularly in market-based methods - is increasingly debated due to the uncertainty in emission reduction verifiability, especially when GCs are involved. As discussed by Bjørn et al., the perceived reduction in emissions attributed to certificate-based instruments may not correspond to real-world changes in renewable energy generation, thereby undermining the credibility of environmental claims[42]. A key distinction lies between bundled and unbundled GCs. Bundled GCs - which are sold together with the physical electricity - are generally regarded as credible, since the renewable attributes are inseparably linked to actual electricity delivery. By contrast, unbundled GCs, which are traded independently of the physical electricity, raise greater concern. Once decoupled, the purchaser cannot verify whether the claimed emission reductions occurred in parallel with actual energy consumption, resulting in potential overestimation of GHG benefits[43,44]. At a given site and year, a company may calculate its Scope 2 GHG emissions using either the market-based or location-based method, as defined in the GHG Protocol. Market-based accounting reflects contractual electricity purchases, such as those backed by GCs, calculated by Equation (1)[44]:

where Emb,S2 refers to market-based (mb) Scope 2 (S2) emissions, CGC refers to electricity consumption covered by GCs, EFGC refers to emission factor of GCs, and (C - CGC) refers to uncovered electricity consumption, and EFres refers to emission factor of residual mix.

Location-based accounting uses the average emission intensity of the local grid, regardless of contract type, calculated by Equation (2)[44]:

where Elb,S2 refers to location-based (lb) Scope 2 (S2) emissions, and EFmix refers to average emission factor for the grid mix.

These methods can yield significantly different results, especially when unbundled GCs are used. Equation (1) captures contractual claims; Equation (2) reflects physical grid impact. Both are relevant in LCA and GHG reporting, but must be applied consistently to avoid misinterpretation.

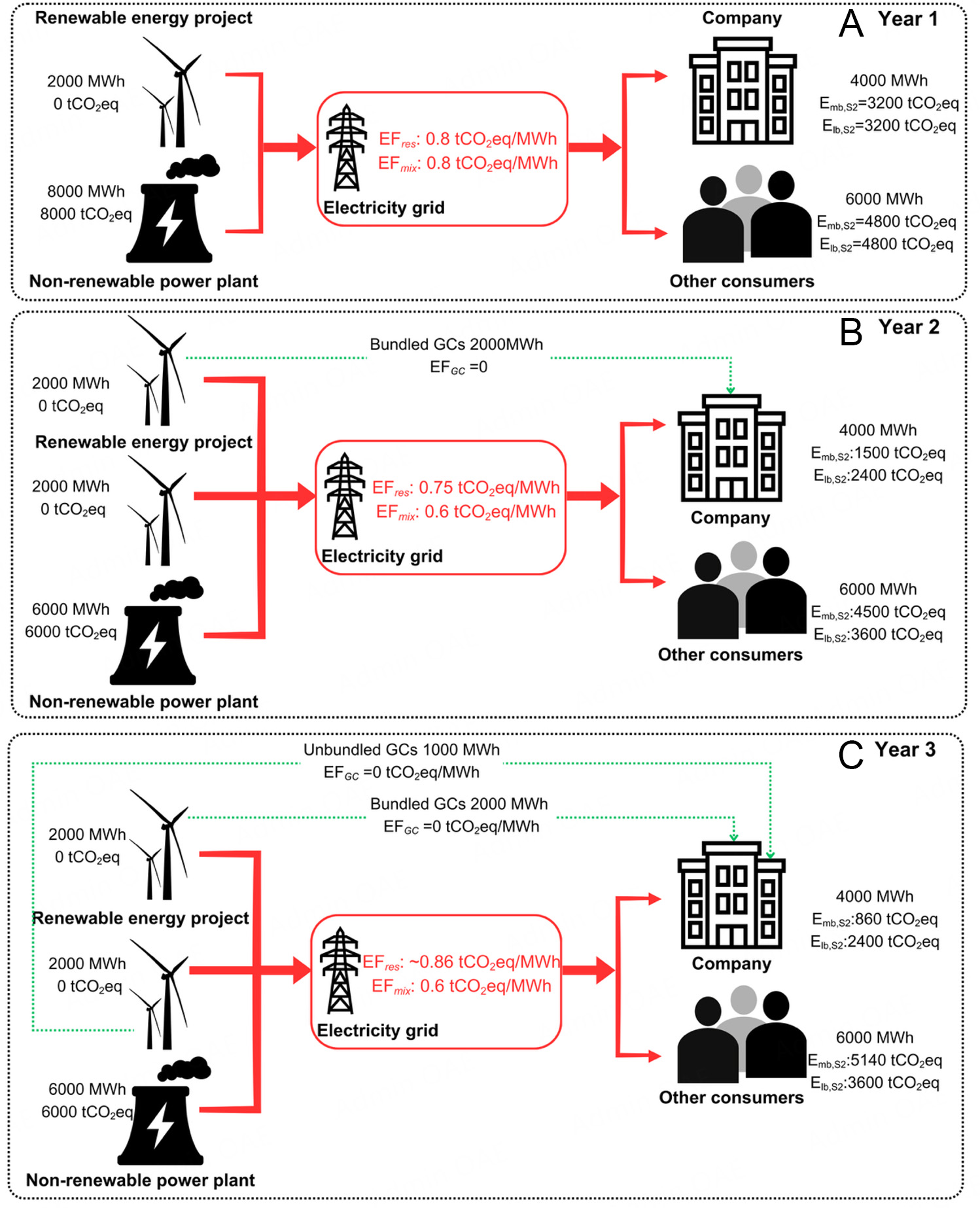

To illustrate the impact of bundled vs. unbundled GCs on reported GHG emissions, Figure 7 simulates three accounting scenarios for a company operating a single facility over three consecutive years:

Figure 7. Three scenarios of one company’s electricity consumption. (A): year 1 - Company without purchasing any GCs; (B): year 2 - Company with purchasing bundled GCs; (C): year 3 - Company with purchasing bundled and unbundled GCs. The icon was created via www.canva.com.

• Year 1: The company purchases grid electricity with no GCs, leading to market-based and location-based emissions both reported at 3,200 tCO2eq/year, assuming an emissions factor of 0.8 tCO2eq/MWh.

• Year 2: The company procures bundled GCs for 2,000 MWh of its total 4,000 MWh consumption, with

• Year 3: Compared to Year 2, the energy structure of the system does not undergo any substantial transformation, as renewable generation remains constant at 4,000 MWh and non-renewables at

The results underscore the risk: while the company’s market-based emissions appear to improve, the location-based emissions - grounded in actual grid intensity - show no further gains beyond the first renewable procurement shift. This gap reflects the reduced validity and traceability of unbundled GCs and raises questions about the actual climate benefit claimed. Furthermore, bundled GCs and similar contractual instruments such as Power Purchase Agreements (PPAs) provide a stronger link between electricity consumption and renewable energy production, improving transparency and traceability. In contrast, the decoupled nature of unbundled certificates challenges their credibility in reflecting tangible emission reductions.

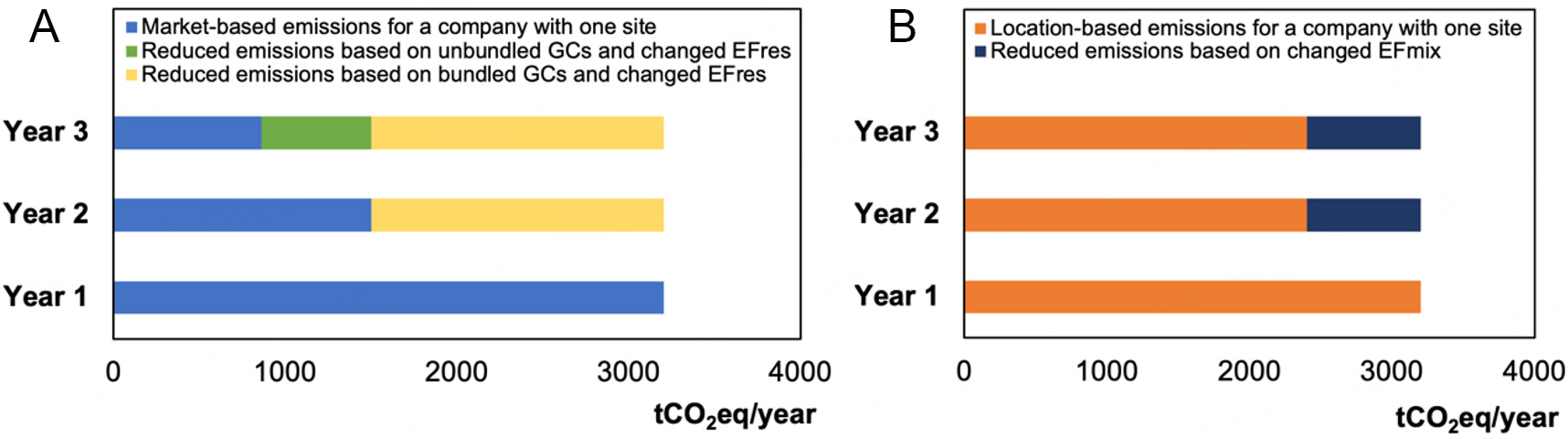

To further clarify the differences between accounting approaches, Figure 8 visually compares the annual CO2eq and their respective reductions across three consecutive years using market-based and location-based methods. Both methods are benchmarked against Year 1, when the company operated without any GCs. Figure 8A presents the market-based emissions. In Year 2, the reduction (shown in yellow) is largely due to bundled GCs and the lower emission factor. In Year 3, a further drop is observed, now including unbundled GCs (green section), which adds to the emission reduction total despite no further change in actual electricity sourcing or generation. The blue segment indicates the reported market-based emissions, which decline steeply over time, though this reduction reflects contractual instruments rather than physical decarbonization. Figure 8B shows location-based emissions. The reductions (shown in orange) are solely tied to the gradual shift in the grid mix, not influenced by market transactions. From Year 1 to Year 2, emissions decrease modestly, due to a higher share of renewables in the regional electricity mix. In Year 3, the emission value remains the same as Year 2, because no further grid-level improvements occurred - even though the company purchased more GCs. While market-based accounting can reflect strategic purchases and branding efforts (e.g., bundled and unbundled GCs), location-based accounting offers a stable reflection of actual grid decarbonization. From a data validity perspective, the discrepancy between claimed reductions (via GCs) and system-level changes becomes apparent. The market-based method is flexible but vulnerable to overestimation, particularly when unbundled GCs are used without a verifiable linkage to the actual electricity supply. On the other hand, the location-based method may underrepresent company efforts but provides a more grounded assessment of emissions as tied to the physical power system. Therefore, organizations should carefully balance these approaches. For reporting purposes, market-based metrics may support brand differentiation and voluntary commitments, but for LCA, policy assessments, or science-based targets, location-based indicators may offer higher credibility and transparency.

Figure 8. Market-based (A) and location-based (B) accounting for annual CO2eq and their relevant reduced emissions compared to the base year (Year 1).

Lack of harmonized guidance on GCs in LCA methodologies

Despite being the global reference, the ISO 14040 and ISO 14044 standards leave substantial room for interpretation[21,28]. Frischknecht and Itten reported that neither ISO 14040 nor ISO 14044 specifies or even mentions the GCs rules when applying them to a product or company LCA study. For example, ISO 14044 only suggests using the “actual electricity production mix in order to reflect the various sources of resources consumed”. However, no further guidance information is defined on whether GCs can be employed in the determination of the “actual production mix”. Additionally, ISO 14067 acknowledges that renewable power can be considered in product carbon footprint calculation with verifiable proof, which opens the door for applying GCs in carbon emission disclosure via LCA. Meanwhile, it also warns against double counting caused by GCs, requiring transparent documentation of certificate ownership and retirement. Similarly, ISO 14064-1:2018 and ISO 14064-2:2019 clarify that such GHG emission reporting could be based on contractual instruments such as GCs, and if GCs are sold, the right to claim the associated emission reductions should be relinquished[45,46]. This flexibility enables broad application but leads to inconsistencies in practice - especially for electricity-related emissions and GC integration. As reported by practitioners, the ISO framework lacks sufficient guidance for ensuring comparability across studies[29]. To improve consistency, the EU’s Product Environmental Footprint (PEF) and Environmental Product Declaration (EPD) frameworks introduce stricter rules[47,48]. However, these approaches also face criticism: (1) PEF’s rules vary by product category and often diverge from international standards, and (2) EPDs suffer from inconsistent treatment of carbon, allocation, and electricity modeling. In both cases, increased complexity does not always translate into better quality or credibility. Then, on the OpenLCA platform, it is recommended that GCs be used to report the GWP instead of location-based methods. Furthermore, given the implicit rules from international standards, OpenLCA proposed that the LCA practitioner should disclose the carbon emissions with or without the renewable energy contract and details of the renewable energy contract applied[49]. Overall, applying GCs, such as GOs, in LCA presents several methodological challenges. First, international standards like ISO 14040 and ISO 14044 provide no explicit guidance on how certificates should be treated, leading to inconsistent practices and undermining comparability across studies. Second, the delinkage of GCs from physical electricity flows creates a risk of double counting, particularly when market-based and location-based approaches are applied in parallel. Third, LCA results are highly sensitive to electricity modeling choices: switching from a production mix to a residual mix can drastically alter outcomes, with some countries experiencing multi-thousand-percent increases in reported impacts. Finally, while GCs are intended to enhance transparency in renewable electricity consumption, their inconsistent application in LCA raises credibility concerns for environmental product declarations, carbon footprint, and policy frameworks such as the EU Taxonomy and Carbon Border Adjustment Mechanism. Together, these issues highlight the urgent need for harmonized methodological guidance on integrating GCs into LCA to ensure robustness and comparability of results[50,51].

Market and policy influences

The implementation of TGCs has grown globally - across regions such as North America, Europe, and Asia - yet the system’s performance remains uneven. Market inefficiencies, policy fragmentation, and region-specific renewable development have limited the effectiveness of GCs as a climate policy tool[52,53]. As shown in Table 2, trading models vary widely - from unbundled transactions in the EU to more mixed systems in China and the U.S. - often shaped by national regulatory priorities and quota mechanisms[54].

TGC trading models and policies in the EU, China, and the U.S.[52]

| Countries | Trading types | Relative policies |

| EU | Unbundled transaction | GOs, an official system with quota requirements and sanctions, etc. |

| U.S. | Bundled and unbundled transaction | Unbundled RECs, power purchase agreements, etc. |

| China | Bundled and unbundled transaction | Green electricity certificate (GEC) and quota obligations |

In markets where uniform certificate pricing is applied regardless of the renewable source, distortions arise. Investors tend to favor the lowest-cost technologies, which risks overconcentration in certain sectors and underinvestment in others. For instance, offshore wind farms are now among the cheapest energy projects in Europe[55], but their weather dependence can cause TGC markets to swing between oversupply and scarcity - undermining certificate reliability and investor confidence. To stabilize these dynamics, scholars have proposed the use of benchmark prices and technology-specific conversion coefficients as quasi-regulatory tools[56]. These would reflect the differing costs, risks, and contributions of various renewables within the TGC framework.

Meanwhile, alignment between GCs and environmental assessment standards is still evolving. While ISO 14040-44 and the GHG Protocol remain foundational, standards like ISO 14064-1:2018 now explicitly allow GCs to be included in organizational GHG inventories and LCA studies[32,33,36,45]. Other instruments - such as EPDs, corporate sustainability reports, and initiatives like the Science Based Targets initiative (SBTi) - also allow the inclusion of GCs to substantiate renewable energy claims, often backed by LCA-based evidence[57], as summarized in Table 3. Nevertheless, methodological gaps and inconsistencies persist across these frameworks. Challenges include unclear allocation rules, inconsistent treatment of electricity modeling, and a lack of harmonized reporting practices - particularly when certificates are traded across borders. Without stronger coordination between market mechanisms and LCA-based standards, the environmental integrity of GCs will remain contested.

Standards and reporting practices related to GCs in LCA

| Standard | Relevant content |

| ISO 14025[58] | Details principles and procedures for developing EPDs, which can include GCs |

| ISO 14040[31] | Provides principles and framework for LCA |

| ISO 14044[32] | Specifies requirements and guidelines for LCA, including data collection and impact assessment |

| ISO 14064-1:2018[45] | Allows organizations to include GCs in their environmental reporting and LCA. Includes provisions for using GCs in GHG inventories |

| ISO 14067[38] | Specifies principles and guidelines for quantifying and reporting the carbon footprint of products, which can include GCs |

| EN 15804[59] | Establishes standards for making EPDs of construction products, which can incorporate GCs |

| GHG Protocol[60] | Offers standards and guidance for quantifying and reporting GHG emissions, including guidelines for accounting for GCs |

| Practice | Relevant content |

| EPDs[58] | Use renewable energy covered by RECs in EPDs and adhere to relevant regulations such as ISO 14025 |

| Corporate sustainability reporting[61] | Reports the use of renewable energy and related environmental benefits while conforming to criteria like ISO 14064 and the GHG Protocol |

| SBTi[57] | Only bundled GCs can be used in LCA |

FRAMEWORK FOR STANDARDIZING GCs IN LCA

In the existing literature, researchers have highlighted several limitations in the current application of GCs within LCA. Some point to incompleteness and inconsistency in related standards and regulations[29,62,63], while others focus on the instability of TGC markets, which undermines the reliability of the trading system itself[64-66]. More recently, studies have examined the methodological dilemmas in GHG quantification and LCA modeling when GCs are involved[39]. Among these contributions, two persistent issues emerge: (1) the risk of double counting renewable electricity attributes; and (2) the lack of verifiability associated with unbundled GCs. Despite these insights, no existing study provides a comprehensive framework for standardizing the use of GCs in LCA - one that connects regulatory guidance, market dynamics, and accounting methodologies.

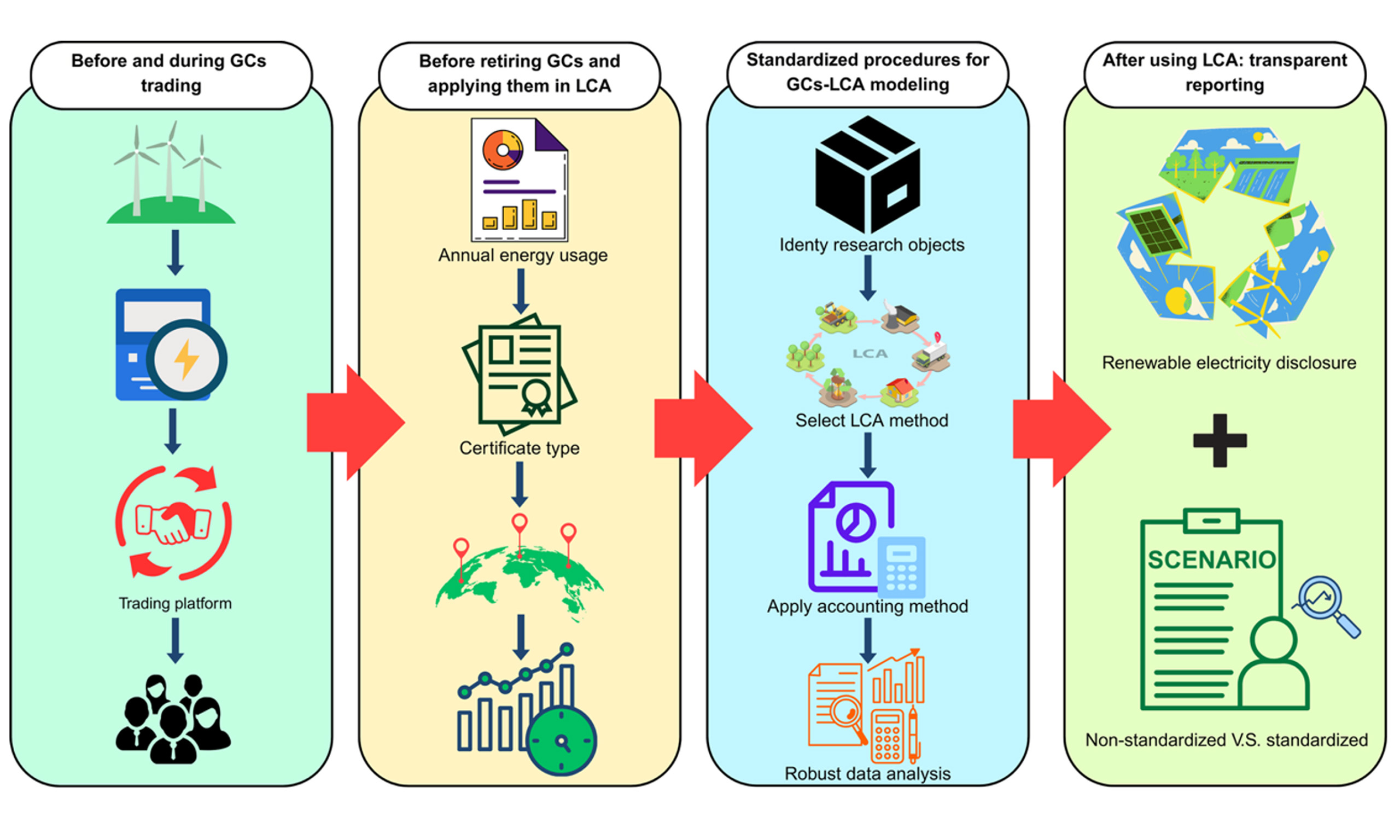

Building on the challenges identified in Chapter 3, Chapter 4 outlines a stepwise framework to improve consistency and transparency in GC application within LCA, from renewable energy generation to final inventory reporting. This includes mechanisms for GC validation, transaction traceability, LCA integration, and result verification.

Ensuring credible use of GCs before and during trading

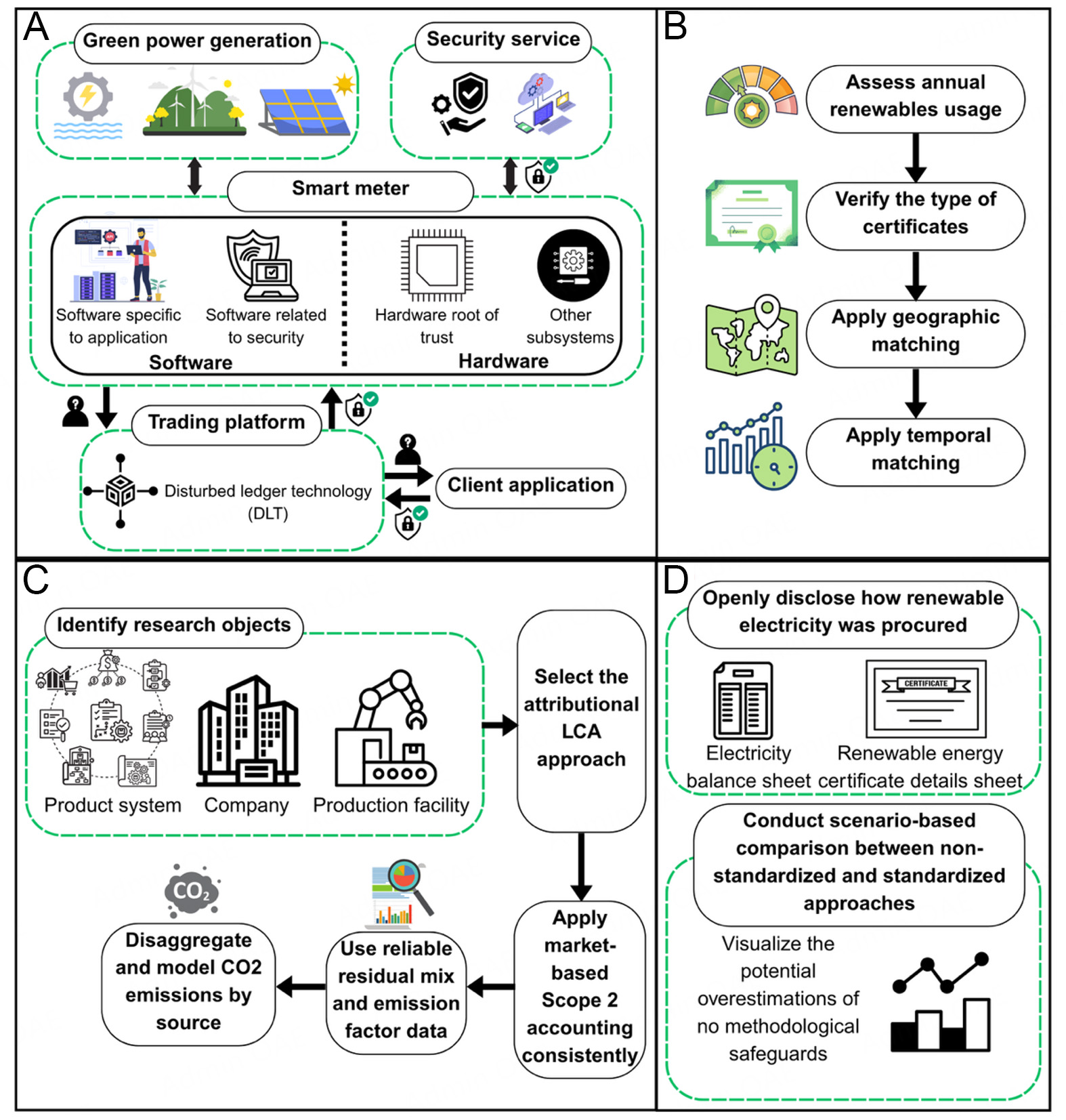

A robust GC system must begin with the trustworthy, tamper-resistant recording of renewable electricity generation. As emphasized by Karakashev et al., the credibility of GCs hinges not only on formal verification but also on the technical integrity of the infrastructure behind their issuance[67]. Without such a foundation, the system remains vulnerable to double issuance, fraud, and unverifiable claims - all of which undermine its use in LCA and GHG reporting. Figure 9A outlines a prototype architecture comprising smart metering, distributed ledger technology (DLT), and secure trading mechanisms - designed to enforce traceability from generation to transaction. The process includes: (1) At the generation site, electricity output is continuously recorded by smart meters equipped with a Trusted Computing Base (TCB). This hardware-enforced trust anchor ensures that the data - especially the association between the energy produced and its renewable source - are authentic and immutable. TCB integration also allows for real-time monitoring and secure authentication, reducing the risk of manipulation at the edge level; (2) Once green electricity is verified, corresponding GCs are logged onto a decentralized ledger, such as a blockchain. DLT enables a non-repudiable and tamper-proof audit trail, which prevents the risks of double spending, forgery, or retroactive alteration of certificate records. This mechanism is particularly critical when GCs are to be traced across multiple actors and jurisdictions; (3) The final step involves the trading of GCs through encrypted client applications. The platform supports anonymized transactions, protecting buyer identity while preserving full transaction traceability. This dual requirement - confidentiality and accountability - is key to building trust among market participants and external verifiers (e.g., auditors or LCA practitioners).

Figure 9. Summary of framework for standardizing GCs applications in LCA: (A) ensure credible use of GCs before and during trading; (B) before retiring GCs and applying them in LCA; (C) standardized procedures for applying GCs in LCA modeling; and (D) verify reporting transparency after using LCA. The icon was created via www.canva.com.

Before retiring GCs and applying them in LCA

As shown in Figure 9B, before incorporating GCs into LCA or GHG reporting, companies must take structured steps to ensure the certificates are valid, relevant, and traceable to actual renewable electricity usage. Failure to do so risks misrepresenting environmental performance and undermining the credibility of Scope 2 emissions disclosures. First, to determine how many GCs can be legitimately retired, companies should calculate their total annual renewable electricity consumption - including both on-site (self-generated) and off-site (purchased) sources. Only the amount of electricity consumed internally may be claimed through GCs. If on-site electricity is sold to third parties, the corresponding GCs cannot be used toward the company’s own carbon disclosures or LCA studies. While most reporting systems rely on annual matching, emerging frameworks may recommend hourly matching or other higher-resolution models in the future. This reinforces the importance of aligning with the latest guidance from regulatory or certification bodies. Second, prioritize the use of bundled GCs, which are delivered with physical electricity, as they offer better traceability and environmental integrity. In contrast, unbundled certificates, which are traded independently, should only be used if no bundled options are available - and even then, their use must be disclosed transparently in LCA datasets. Third, only use certificates that originate from the same country or regional market in which electricity is consumed. This geographic alignment ensures the environmental attributes of the certificate are regionally relevant. For example, a company based in France may use European GOs, but cannot claim renewable electricity from RECs in North America or green electricity certificates (GECs) in China, as these operate under separate frameworks and assumptions. Finally, ensure that the GCs being retired were generated within a valid timeframe, typically during or just prior to the reporting year. Certificates that are traded before the actual electricity generation - a known issue in some unbundled GC markets - should be excluded. GCs should only be used if they are not expired and clearly linked to verified, completed energy production.

Standardized procedures for applying GCs in LCA modeling

When incorporating GCs into LCA, it is essential to follow a structured, transparent methodology that aligns with both LCA principles and Scope 2 accounting rules. Figure 9C summarizes a five-step process to ensure consistency and prevent misinterpretation when modeling environmental impacts linked to GC-based electricity: Step 1 clearly defines the subject of the LCA - be it a company, production facility, or product system. This sets the boundary conditions for data collection and determines how electricity usage and GC retirement are allocated within the assessment. Step 2 selects the attributional LCA approach, considering that GCs reflect contractual electricity claims. It enables the inclusion of supplier-specific electricity data and aligns reporting requirements under schemes such as EPDs and corporate GHG inventories. Step 3 applies market-based Scope 2 accounting consistently to avoid double counting of renewable electricity across organizational units or product boundaries. Fragmented or hybrid use of both market- and location-based methods within the same LCA model can compromise transparency and data integrity. Step 4 uses reliable residual mix and emission factor data sourced from country-specific, annually updated datasets that exclude imports or exports of GCs. For instance, while an EU-wide average for GOs may exist, using it in national-level Scope 2 or product reporting introduces allocation errors and geographic mismatches. Step 5 disaggregates and models CO2 emissions by source: (1) consumption covered by GCs, and (2) remaining consumption covered by the residual mix. Each is assigned its respective emission factor. This separation is essential for transparent reporting and avoids masking fossil-based electricity under an averaged figure.

After using LCA: toward verifiable and transparent impact reporting

Once GCs have been applied in LCA, the credibility of the results relies not only on the modeling approach itself but also on how the outcomes are reported, justified, and verified. Without clear post-modeling procedures, even a technically correct LCA may fall short in traceability, transparency, or stakeholder trust. Central to this phase is the requirement for transparent reporting. As presented in Figure 9D, companies must openly disclose how renewable electricity was procured - whether through bundled certificates, direct purchases, or PPAs - and clearly state the source and type of each certificate. This transparency is vital for distinguishing between credible climate action and unverifiable claims.

To reinforce data reliability, the LCA report should also include an electricity balance sheet (see Supplementary Table 1), detailing total electricity consumption, GC allocation across life cycle stages, and the regional and temporal attributes of both conventional and renewable electricity sources[41]. This accounting helps verify whether the renewable electricity matches the claimed usage period and whether GCs are correctly allocated without exceeding the actual consumption. Additionally, the background documentation must contain certificate-level metadata (see Supplementary Table 2), such as the renewable generator’s identity, generation dates, tracking ID, and geographic location[41]. Including this information ensures traceability and confirms compliance with key criteria such as geographic matching, valid timeframes, and generation authenticity - especially relevant when unbundled certificates are used.

To critically evaluate the effect of standardized GC application in LCA, companies are encouraged to conduct scenario-based comparisons. These can highlight the differences in reported emissions between non-standardized and standardized approaches, such as using no GCs, only bundled GCs, or a mix of bundled and unbundled GCs with and without verification steps. Through these comparisons, it becomes possible to visualize the magnitude of potential overestimations when methodological safeguards are absent. Plotting CO2 outcomes across scenarios also reinforces how proper standardization can significantly improve the credibility and reproducibility of reported environmental benefits. Ultimately, this post-LCA stage plays a pivotal role in closing the accountability loop. It demonstrates that renewable electricity claims, when supported by rigorous data management and standardized certificate practices, can move beyond symbolic reporting and contribute meaningfully to verified climate impact reduction.

POLICY AND REGULATORY RECOMMENDATIONS FOR CREDIBLE CLIMATE CLAIMS

Despite the increasing integration of GCs into environmental reporting and LCA, their effectiveness is still hindered by regulatory fragmentation, market instability, and methodological inconsistencies. This chapter proposes a set of policy and governance recommendations to address the core gaps identified in our review.

Governance, verification, and claim clarity

Strengthening the governance of certificate issuance and claims is fundamental. To ensure environmental credibility, organizations should be required to retire GCs before making any renewable energy or emissions reduction claims. Third-party verification - such as via the Green-e certification in North America - should become standard to reduce greenwashing and promote accountability[68]. Furthermore, companies must specify both the share and source of their renewable electricity. For example, rather than stating they are "powered by renewables", firms should report that “60% of our manufacturing facilities are powered by solar energy.” Such precision enhances both comparability and public trust.

The GHG Protocol remains the most influential framework for corporate carbon accounting, particularly in guiding how GCs are used to report Scope 2 emissions. However, its current endorsement of market-based accounting - particularly when applied through GCs - has drawn substantive criticism from both academia and civil society. NGOs such as Greenpeace contend that GCs often fail to uphold environmental integrity due to a lack of additionality (i.e., certificates not linked to new renewable capacity), transparency in procurement and use, and traceability in tracking energy origin and impact[69]. These shortcomings call into question the legitimacy of emissions reductions claimed through certificate purchases alone.

A fundamental issue lies in the reallocation rather than the reduction of emissions. When firms purchase GCs, the renewable electricity they claim is subtracted from the regional residual mix, effectively increasing the average carbon intensity for all other users who rely on the same grid. This substitution effect can create a misleading picture of climate progress - where reductions on paper for one actor come at the expense of others - resulting in no net global decarbonization. In this sense, the current GHG Protocol approach risks perpetuating zero-sum accounting that undermines systemic goals. To address these pitfalls, the GHG Protocol must critically reassess its treatment of GCs, especially with respect to system-level emission consequences. A number of interlinked structural reforms are warranted:

• Cross-border harmonization of certificate issuance and recognition rules, particularly within transnational schemes like the EECS, is vital to eliminate inconsistencies and regulatory loopholes[70].

• The creation of transparent, auditable, and user-friendly trading platforms is necessary to prevent double counting, enable traceability, and reinforce market confidence in GC transactions.

• A shift toward temporal granularity - matching certificates to electricity use in real time or near-real time - is essential. The current reliance on annual or even monthly matching is increasingly inadequate, as it ignores the intermittency of renewables and creates artificial congruence between supply and demand.

• Open access to high-resolution GC data should be made a minimum requirement for integration into corporate LCA and sustainability reporting. This would allow independent verification and ensure consistency across datasets.

These shortcomings are not merely theoretical. As evidenced by hourly data from companies like Google, even enterprises that purchase significant amounts of green electricity continue to experience temporal supply gaps, especially during periods when solar or wind generation is unavailable. The mismatch between certificate issuance and actual clean energy consumption highlights the need for real-time certificate validation as a more honest and effective way to account for Scope 2 emissions. Failing to implement such changes risks turning GCs into tools for optical compliance, rather than mechanisms that drive meaningful environmental impact. Therefore, without significant reform, the GHG Protocol’s current endorsement of GC-based accounting may paradoxically enable greenwashing, while impeding the very decarbonization efforts it was designed to support.

Stabilizing the TGC market: from price signals to smart design

The efficiency of the TGC market itself is another major concern. Trading volatility, uniform pricing across technologies, and low transparency all reduce investor confidence and environmental impact. To improve functionality, Yi et al. (2020) propose introducing benchmark prices and conversion coefficients that reflect real technology costs and system contributions[71]. Moreover, price modeling based on willingness to pay (WTP) and ability to pay (ATP) provides a more adaptive pricing framework. Wimmers and Madlener suggest a layered model that accounts for both consumer preference and economic capability, grounded in national statistics. This model allows for dynamic pricing of GCs that supports both economic efficiency and equitable access[72].

Toward a harmonized and interoperable GC system

Currently, no global GC standard exists. National systems - such as GOs (Europe), RECs (U.S.), I-RECs (developing countries), and GECs (China) - differ significantly in scope, eligibility, and credibility. This fragmentation impedes the development of a global renewable electricity market and limits the ability of companies operating internationally to consolidate environmental claims. There is a strong case for harmonizing certification schemes across regions, possibly under a shared standard such as RE100, which already recognizes GOs, RECs, I-RECs, and APX-TIGRs. RE100 offers a model for voluntary international alignment and could serve as a stepping stone toward a globally recognized GC framework that supports LCA and Scope 2 accounting[72]. As energy markets become more integrated, and as digital tools allow for finer temporal and spatial tracking, international coordination on GC governance will become essential for the credible and efficient scaling of green electricity markets.

CONCLUSION AND FUTURE DIRECTION

This review critically examined the integration of GCs into LCA, with a focus on methodological inconsistencies, regulatory gaps, and market-based accounting frameworks. As the global demand for renewable energy accountability rises, GCs have become a dominant tool for communicating environmental performance, particularly under the GHG Protocol. However, this study finds that their application in LCA is still far from standardized, and in many cases, lacks scientific robustness. Key findings reveal two major systemic concerns: (a) the risk of double counting, especially in uncoordinated and cross-border trading systems; and (b) the questionable verifiability of unbundled certificates, which undermines environmental credibility. Although instruments like the PEF and EPDs offer structure, their application to GCs remains underdeveloped and fragmented across product categories and geographies.

Moreover, this review proposes a structured workflow for applying GCs in LCA - from generation and trading, through temporal and geographic screening, to final allocation and impact modeling. This framework not only enhances transparency but also serves as a practical reference for LCA practitioners and sustainability professionals navigating GC-based reporting. On the policy side, several pressing needs emerged: revisiting how the GHG Protocol handles system-wide emissions shifts, harmonizing international certification schemes, enforcing temporal matching, and requiring more granular certificate data disclosure. Furthermore, the volatility and inefficiencies of TGC markets call for the introduction of benchmark pricing models and willingness-to-pay-based pricing strategies.

Despite its comprehensive scope, the study has limitations. It adopts a phased, thematic literature review rather than a quantitative bibliometric analysis. While this approach allows for an in-depth exploration of methodological debates, it inevitably introduces a degree of subjectivity in the selection and interpretation of sources. Future research could complement these findings with systematic, quantitative analyses to provide a more objective overview of developments in the field. The framework proposed is conceptual and needs validation through real-world corporate case studies. Regional nuances in regulatory practice may also limit the global transferability of some recommendations. Still, the work opens new research directions - such as modeling hourly GC matching impacts, evaluating supply-chain-wide renewable energy flows, or exploring blockchain-based verification systems for RECs. It is thus essential for GCs to evolve from a symbolic gesture to a credible mechanism of climate action, with both methodological clarity and policy reform.

To further strengthen the credibility of GCs in assessments and environmental declarations, future research should focus on developing reliable tracking systems using programming and data analysis, and applying AI and blockchain to modernize GC trading. Another key direction is to design mechanisms that integrate GCs from various renewable sources into future low-carbon energy portfolios. These efforts will support more accurate global carbon accounting and verifiable emission reductions.

DECLARATIONS

Acknowledgements

Meng, X. gratefully acknowledges the financial support from the scholarship of the School of Environment, Tsinghua University, and the Global Degree Scholarship of the University of Padova.

Authors’ contributions

Made substantial contributions to the conception and design of the study and performed data analysis and interpretation: Meng, X.; Wu, J.

Performed data acquisition, as well as providing administrative, technical, and material support: Zhang, Y.; Ren, J.; Yue, D.; Manzardo, A.

Availability of data and materials

Not applicable.

Financial support and sponsorship

This work was financially supported by the scholarship of the School of Environment, Tsinghua University, and the Global Degree Scholarship of the University of Padova.

Conflicts of interest

Ren, J. is the Associate Editor of Carbon Footprints. He had no involvement in the review or editorial process of this manuscript, including but not limited to reviewer selection, evaluation, or the final decision, while the other authors have declared that they have no conflicts of interest.

Ethical approval and consent to participate

Not applicable.

Consent for publication

Not applicable.

Copyright

© The Author(s) 2025.

Supplementary Materials

REFERENCES

1. Rose, A.; Wei, D.; Miller, N.; Vandyck, T. Equity, emissions allowance trading and the Paris agreement on climate change. EconDisCliCha 2017, 1, 203-32.

2. Garvens, H. J.; Albrecht, S.; Fischer, M.; Scagnetti, C.; Barkmeyer, M.; Braune, A. Transfer towards climate neutrality - from LCA to a business case. E3S. Web. Conf. 2022, 349, 07002.

3. EMBER. Yearly electricity data. Available from: https://ember-climate.org/data-catalogue/yearly-electricity-data/ [Last accessed on 13 Oct 2025].

4. Energy Institute. Statistical review of world energy. Available from: https://www.energyinst.org/statistical-review/ [Last accessed on 13 Oct 2025].

5. Vertes, A. A.; Qureshi, N.; Blaschek, H. P.; Yukawa, H. Green energy to sustainability: strategies for global industries. John Wiley & Sons; 2020.

6. RECS Energy Certificate Association. Maximising the reliability and impact of buying renewables: guidance for market participants. Available from: https://recs.org/news/recs-international-publishes-guidance-for-market-participants/ [Last accessed on 13 Oct 2025].

7. Safarzadeh, S.; Hafezalkotob, A.; Jafari, H. Energy supply chain empowerment through tradable green and white certificates: a pathway to sustainable energy generation. Appl. Energy. 2022, 323, 119601.

8. Akerlof, G. A. 15 - The market for “lemons”: quality uncertainty and the market mechanism. In Uncertainty in Economics. Academic Press; 1978, pp 235-51.

9. De Matos, T. F. Certificados de energia renovável - conceituação através de uma revisão sistemática de literatura. Revista. Gesta. 2024, 12.

10. Mondello, G.; Salomone, R. Chapter 10 - Assessing green processes through life cycle assessment and other LCA-related methods. In: Studies in surface science and catalysis; 2020. pp. 159-85.

11. Kåberger, T.; Karlsson, R. Electricity from a competitive market in life-cycle analysis. J. Clean. Prod. 1998, 6, 103-9.

12. Amundsen, E. S.; Mortensen, J. B. The Danish Green Certificate System: some simple analytical results. Energy. Econ. 2001, 23, 489-509.

13. Amundsen, E. S.; Bergman, L. Green certificates and market power on the nordic power market. Energy. J. 2012, 33, 101-18.

14. Linares, P.; Santos, F. J.; Ventosa, M. Coordination of carbon reduction and renewable energy support policies. Clim. Policy. 2008, 8, 377-94.

15. THEMA. Available from: https://thema.no/en/news-and-publications/ [Last accessed on 13 Oct 2025].

16. The European Parliament and the Council of the European Union. Directive 2001/77/EC of the European Parliament and of the Council of 27 September 2001 on the promotion of electricity produced from renewable energy sources in the internal electricity market; 2001, pp. 33-40. Available from: http://data.europa.eu/eli/dir/2001/77/oj [Last accessed on 13 Oct 2025].

17. The European Parliament and the Council of the European Union. Directive 2009/28/EC of the European Parliament and of the Council of 23 April 2009 on the promotion of the use of energy from renewable sources and amending and subsequently repealing Directives 2001/77/EC and 2003/30/EC (Text with EEA relevance); 2009, pp. 16-62. Available from: http://data.europa.eu/eli/dir/2009/28/oj [Last accessed on 13 Oct 2025].

18. The European Parliament and the Council of the European Union. Directive (EU) 2018/2001 of the European Parliament and of the Council of 11 December 2018 on the promotion of the use of energy from renewable sources (recast) (Text with EEA relevance.); 2018, pp. 82-209. Available from: http://data.europa.eu/eli/dir/2018/2001/oj [Last accessed on 13 Oct 2025].

19. European Commission. Fit for 55: delivering on the proposals. Available from: https://commission.europa.eu/strategy-and-policy/priorities-2019-2024/european-green-deal/delivering-european-green-deal/fit-55-delivering-proposals_en [Last accessed on 13 Oct 2025].

20. The European Parliament and the Council of the European Union. Directive (EU) 2023/2413 of the European Parliament and of the Council of 18 October 2023 amending Directive (EU) 2018/2001, Regulation (EU) 2018/1999 and Directive 98/70/EC as regards the promotion of energy from renewable sources, and repealing Council Directive (EU) 2015/652; 2023. Available from: https://data.europa.eu/eli/dir/2023/2413/oj [Last accessed on 13 Oct 2025].

21. European Commission. Implementing and delegated acts - CSRD. Available online: https://finance.ec.europa.eu/regulation-and-supervision/financial-services-legislation/implementing-and-delegated-acts/corporate-sustainability-reporting-directive_en [Last accessed on 13 Oct 2025].

22. European Union. Directive (EU) 2025/794 of the European Parliament and of the Council of 14 April 2025 amending Directives (EU) 2022/2464 and (EU) 2024/1760 as regards the dates from which Member States are to apply certain corporate sustainability reporting and due diligence requirements (Text with EEA relevance); 2025. Available from: http://data.europa.eu/eli/dir/2025/794/oj [Last accessed on 13 Oct 2025].

23. European Commission. European hydrogen bank, 16 March 2023. Available from: https://energy.ec.europa.eu/topics/eus-energy-system/hydrogen/european-hydrogen-bank_en [Last accessed on 13 Oct 2025].

24. Sustainability Impact Metrics. Guarantees of origin, renewable energy certificates, the residual mix and carbon offsetting in LCA. Available from: https://www.ecocostsvalue.com/lca/gos-and-recs-in-lca/ [Last accessed on 13 Oct 2025].

25. Greenhouse Gas Protocol. Available from: https://ghgprotocol.org/ [Last accessed on 13 Oct 2025].

26. CDP. Available from: https://www.cdp.net/zh [Last accessed on 13 Oct 2025].

27. RE100. Available from: https://www.there100.org/ [Last accessed on 13 Oct 2025].

28. European Commission. Revision of the energy taxation directive: questions and answers; 2021. Available from: https://ec.europa.eu/commission/presscorner/detail/en/qanda_21_3662 [Last accessed on 13 Oct 2025].

29. Association of Issuing Bodies (AIB). Available from: https://www.aib-net.org/eecs/eecsr-rules [Last accessed on 13 Oct 2025].

30. The European Parliament and the Council of the European Union. Directive 2009/72/EC of the European Parliament and of the Council of 13 July 2009 concerning common rules for the internal market in electricity and repealing Directive 2003/54/EC (Text with EEA relevance); 2009, pp 55-93. Available from: http://data.europa.eu/eli/dir/2009/72/oj [Last accessed on 13 Oct 2025].

31. International Organization for Standardization (ISO). ISO 14040:2006 - Environmental management-life cycle assessment-principles and framework; Geneva: ISO; 2006. Available from: https://www.iso.org/standard/37456.html [Last accessed on 13 Oct 2025].

32. International Organization for Standardization (ISO). ISO 14044:2006 - Environmental management-life cycle assessment-requirements and guidelines; Geneva: ISO; 2006. Available from: https://www.iso.org/standard/38498.html [Last accessed on 13 Oct 2025].

33. Brandão, M.; Busch, P.; Kendall, A. Life cycle assessment, quo vadis? Supporting or deterring greenwashing? A survey of practitioners. Environ. Sci. Adv. 2024, 3, 266-73.